TVS Motor Company (TVSL) is a reputed two and three-wheeler manufacturer globally, championing progress through Sustainable Mobility with four state-of-the-art manufacturing facilities in Hosur, Mysuru, and Nalagarh in India and Karawang in Indonesia. Its products lead in their respective categories in the J.D. Power IQS and APEAL surveys. Its group company Norton Motorcycles, based in the United Kingdom, is one of the most emotive motorcycle brands in the world. The company’s subsidiaries in the personal e-mobility space, Swiss E-Mobility Group (SEMG), and EGO Movement have a leading position in the e-bike market in Switzerland. TVS Motor Company endeavors to deliver the most superior customer experience across the 80 countries in which it operates.

| Result Analysis: TVS Motors Company Limited (CMP: Rs. 1306.50) | Result Update: Q1FY24 |

| Stock Details | |

| Market Cap. (Cr.) | 62071.82 |

| Equity (Cr.) | 47.51 |

| Face Value | 1 |

| 52 Wk. high/low | 1385 / 837 |

| BSE Code | 532343 |

| NSE Code | TVSMOTOR |

| Book Value (Rs) | 115.87 |

| Sector | Automobiles |

| Key Ratios | |

| Debt-Equity: | 3.86 |

| ROCE (%): | 13.59 |

| ROE (%): | 26.44 |

| TTM EPS: | 30.69 |

| P/BV: | 11.28 |

| TTM P/E: | 42.57 |

Result Highlights:

-

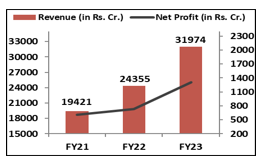

TVSL reported a robust growth in revenue of 23.8% YoY, and 12.8% on sequential basis which was mainly driven by ~5% YoY growth in volumes and ~14% YoY growth in ASP to INR 75.7k per unit.

-

The company reported a record EBITDA of Rs.1,215cr., 13.4% EBITDA margin (+30 bps QoQ; consistent). Commodity prices are anticipated to stay favourable for the upcoming quarters, and as a result, operational leverage advantages and price increases will increase EBITDA margin.

-

PAT was lower by 14% QoQ and 5% YoY basis due to high finance cost, depreciation, and transition to new tax regime.

-

Domestically, TVSL anticipates significant growth in urban markets, but only modest development in rural areas. The delayed monsoon was first concerning, but it now looks usual. The government’s support for high MSP would help the buying mentality in rural regions, as will an equitable distribution of rainfall. The firm increased its market share in the 2W area by 225bps, to 17.42%, driven by a 447bps growth in the motorcycle category.

-

The prognosis for exports remains unclear owing to currency depreciation. However, MoM, retail sales continue to rise. The business keeps its distributor-level inventories at 30-35 days. The majority of the channel destocking has already been completed, and exports are anticipated to increase starting in H2FY24. Export revenue were Rs 16.65 billion, realizing Rs 82 per USD.

-

In the EV segment the industry demand was harmed by the FAME (Faster Adoption and Manufacturing of Electric Vehicles) subsidy decrease in June 23; however, demand started to rebound a little in July 23. Demand is projected to return to normal by 2HFY24. It is increasing iQube production and anticipates attaining a monthly output of about 25k devices. Even with the FAME subsidy decrease and goodwill return (which absorbed negative impacts of 0.2-0.3% against revenue for 30k bookings), the contribution margin in the EV industry is still positive.

-

Company also expects to introduce new EVs in the 5-25kW class in the upcoming months, while the introduction of the e3W is anticipated for H1FY24.

-

Over and beyond the investment objective of Rs8.5-9b (including Rs4b in 1QFY24), Capex is targeted at Rs9-10b (including EV).

-

The cost of debt increased by 0.3%, driving the increase in interest rates, while borrowings also increased by Rs2.5b.

Financial Performance: Shareholding Pattern:

Shareholding Pattern:

| Particulars (In%) | Q1FY23 | Q1FY24 |

| Promoters Group | 50.81 | 50.27 |

| FIIs | 10.18 | 18.45 |

| DIIs | 30.74 | 23.42 |

| Public | 7.76 | 7.37 |

| Others | 0.51 | 0.49 |

Outlook:

TVSL reported inline operating performance. Realizations grew at Rs75.7k/unit for the fifth straight quarter as price increases took the lead. As EV share is projected to rise in the future, QoQ margin improvement will be dependent on RM softening and operating leverage. Price increases persisted with an increase of 0.5% in Q2FY24, 0.8% to 1.0% in May’23, and 1.0% to 1.1% in Q1FY24. Management reiterated EV releases in the future (in the 2W and 3W sectors, with a capacity of 5 to 25 kwh). TVSL is in a better position than other 2W OEMs in both ICE and EVs due to higher product acceptance, which could lead to additional market share increases. TVSL stated that volumes will return to normal by Q3 or Q4 following the latest FAME 2 subsidy cutbacks in EVs.

Results:

| Particulars (In Rs. Cr.) | Q1FY24 | Q4FY23 | Q1FY23 | QoQ% | YoY% |

| Revenue from Operations | 9,056 | 8,031 | 7,316 | 12.8% | 23.8% |

| Other Income | 87 | 67 | 32 | 28.9% | 169.3% |

| Total Income | 9,142 | 8,099 | 7,348 | 12.9% | 24.4% |

| Cost of materials consumed | 5,501 | 4,946 | 4,614 | 11.2% | 19.2% |

| Purchase of Stock-in-Trade | 460 | 136 | 219 | 236.9% | 110.1% |

| Changes in inventories | -272 | 18 | 19 | – | – |

| Employee expense | 821 | 762 | 659 | 7.7% | 24.6% |

| Other Expense | 1,332 | 1,114 | 900 | 19.5% | 48.1% |

| EBITDA | 1,215 | 1,054 | 905 | 15.2% | 34.2% |

| EBITDA Margin (%) | 13.4% | 13.1% | 12.4% | 30 bps | 100 bps |

| Finance Cost | 437 | 398 | 292 | 9.7% | 49.7% |

| Depreciation & Amortisation expense | 227 | 232 | 199 | -2.1% | 14.1% |

| Profit Before Tax (PBT) | 637 | 491 | 447 | 29.8% | 42.7% |

| Tax | 185 | 151 | 139 | 22.7% | 32.9% |

| Exceptional Items-incomes/expenditure | -11 | -4 | 11 | 138.1% | -200.6% |

| Profit After Tax (PAT) | 441 | 336 | 318 | 31.5% | 38.8% |

| PAT Margin (%) | 4.9% | 4.2% | 4.3% | 70 bps | 60 bps |

| EPS (in Rs.) | 9.14 | 7.07 | 6.43 | 29.3% | 42.1% |

| Segment Revenue (In Rs. Cr.) | Q1FY24 | Revenue % | Q4FY23 | QoQ% | Q1FY23 | YoY% |

| Automotive Vehicles & Parts | 7,614 | 83.2% | 6,704 | 13.57% | 6,328 | 20.32% |

| Automotive Components | 189 | 2.1% | 192 | -1.98% | 204 | -7.37% |

| Financial services | 1,351 | 14.8% | 1,235 | 9.37% | 867 | 55.85% |

| Others | 0.02 | 0.0% | 0.01 | 100.00% | 3.77 | -99.47% |

| Total | 9,153 | 100.0% | 8,132 | 12.56% | 7,402 | 23.66% |

Source: Company website, EWL Research

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India.( SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Kiran Tahlani, Elite Wealth Limited, kirantahlani@elitestock.com

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

(1) all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

(2) no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the report.

For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or e-mailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale.

Legal Entities Disclosures

Mr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone: 011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

- Reports

- a) EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

(b) EWL or its associates or relatives, have no actual/beneficial ownership of one per cent. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

(c) EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

- Compensation

(a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

(b) EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

(c) EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(d) EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(e) EWL or its associates have not received any compensation or other benefits from the subject company or third party in connection with the research report.

3 In respect of Public Appearances

(a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

(b) The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL

Provided that research analyst or research entity shall not be required to make a disclosure as per sub-clauses (c), (d) and (e) of clause (ii) or sub-clauses (a) and (b) of clause (iii) to the extent such disclosure would reveal material non-public information regarding specific potential future investment banking or merchant banking or brokerage services transactions of the subject company.

(4) EWL or its proprietor has never served as an officer, director or employee of the subject company;

(5) EWL has never been engaged in market making activity for the subject company;

(6) EWL shall provide all other disclosures in research report and public appearance as specified by the Board under any other regulation