Fusion Micro Finance Limited IPO Company Profile :

Fusion Micro Finance Limited (FMFL), the second largest NBFC-MFI at the end of June 2022 provides financial services to unserved and underserved women in rural and peri-rural areas across India. It is the third fastest growing NBFC-MFI among the top 10 NBFC-MFIs over FY2019-2022. The company was incorporated in 2010 and as of June 30, 2022 the AUM of the company is Rs. 7,389.02 Crores. FMFL has a significant footprint across India, has reached to 29 Lakhs active borrowers which are served through its network of 966 branches and 9,262 permanent employees spread across 377 districts in 19 states and union territories in India. The company’s key product offerings are income-generating loans that provide capital for women entrepreneurs in rural areas to fund businesses operating in the agriculture-allied and agriculture, manufacturing and production, trade and retail, and services sectors.

| IPO-Note | Fusion Micro Finance Limited |

| Rs.350 – Rs.368 per Equity share | Recommendation: A bit overpriced, better to avoid |

Fusion Micro Finance Limited IPO Details:

| Issue Details | |

| Objects of the issue | · To expand the capital of the company.

· To gain the listing benefits. |

| Issue Size | Total issue Size – Rs. 1103.99 Crore

Fresh Issue – Rs. 600 Crore Offer For Sale – Rs. 503.99 Crore |

| Face value | Rs. 10.00 Per Equity Share |

| Issue Price | Rs. 350 – Rs. 368 |

| Bid Lot | 40 shares |

| Listing at | BSE, NSE |

| Issue Opens: | 02nd November, 2022 – 04th November, 2022 |

| QIB | 50% of Net Issue Offer |

| Retail | 35% of Net Issue Offer |

| NII | 15% of Net Issue Offer |

Fusion Micro Finance Limited IPO

Wants To Apply Online

Trade AnyTime AnyWhere With Elite Empower Mobile App

Fusion Micro Finance Limited IPO Financial analysis:

| Particulars | Q1 FY-23(in cr.) | FY-22(in cr.) | FY-21(in cr.) | FY-20(in cr.) | CAGR |

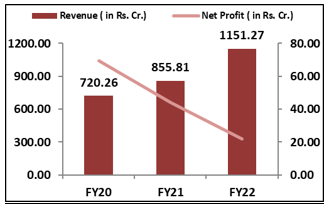

| Revenue from operations | 342.72 | 1151.26 | 855.81 | 720.26 | 16.9% |

| Other Income | 17.72 | 50.08 | 17.27 | 10.04 | |

| Employee Cost | 72.23 | 233.06 | 168.64 | 148.33 | |

| Finance Cost | 143.18 | 495.96 | 375.1 | 337.67 | |

| Impairment on financial instruments | 20.06 | 368.69 | 220.78 | 92.69 | |

| Other expenses | 23.35 | 73.82 | 47.87 | 49.03 | |

| EBITDA | 101.62 | 29.81 | 60.69 | 102.58 | -33.8% |

| EBITDA margin% | 29.65% | 2.59% | 7.09% | 14.24% | |

| Depreciation | 1.47 | 5.37 | 3.89 | 2.57 | |

| PBT | 100.15 | 24.44 | 56.80 | 100.01 | -37.5% |

| Total tax | 25.02 | 2.67 | 12.84 | 30.38 | |

| PAT | 75.13 | 21.77 | 43.96 | 69.63 | -32.1% |

| Dep./revenue% | 0.43% | 0.47% | 0.45% | 0.36% | |

| Int./revenue% | 41.78% | 43.08% | 43.83% | 46.88% |

Check Fusion Micro Finance Limited IPO Allotment Status

Go Fusion Micro Finance Limited IPO allotment status would be available soon after the IPO closure date. Usually the allotment comes within a week from the closing date which in this IPO yet to be announced.

One can check the allotment on the given below link with PAN number or Application number or DP Client Id. All you need to do is to follow these steps:-

- To Fusion Micro Finance Limited IPO Allotment Status

- Go to Application Status

- Select IPO as Fusion Micro Finance Limited IPO

- Enter your PAN Number or Application Id or DP Client Id.

Fusion Micro Finance Limited IPO

Application Form

Fusion Micro Finance Limited IPO Strengths:

-

The company offers an increasing variety of financial products and has deep rooted presence in rural markets across India. As of June 30, 2022, 70.77% of the total customers, 72.05% of the total branches and 91.37% of the total AUM, were from rural areas.

-

The average effective cost of borrowings has declined at a steady rate and was 10.10% for the three months ended June 30, 2022.

-

It has good risk management policies and underwriting processes, such as the extensive customer assessment methodologies and monitoring systems.

- Fusion Micro Finance Limited believes that its customer-centric model and its ability to leverage the extensive distribution network and deep-rooted presence in rural markets across India, make it well-placed to offer a variety of financial products in areas where financial services penetration remains limited. Over the last decade, it has built a deep rural franchise in the microfinance segment. As of June 30, 2022, 2.05 million or 70.77% of the total customers, 696 branches or 72.05% of the total branches, and ₹6,751.19 crore or 91.37% of the total AUM, were from rural areas.

- Fusion Micro Finance Limited has adopted a calibrated approach towards diversifying the fundraising sources and minimizing the costs of borrowings with prudent asset liability management and effective liquidity management. The average effective cost of borrowings of the company has declined at a steady rate and was 10.10%, 10.43%, 11.23%, and 12.33% for the three months ended June 30, 2022, and the financial years 2022, 2021, and 2020, respectively.

- Robust risk management policies and underwriting processes, such as the extensive customer assessment methodologies and monitoring systems, have resulted in healthy portfolio quality indicators. As of June 30, 2022, and March 31, 2022, 2021, and 2020, the gross NPA ratio of the company was 3.67%, 5.71%, 5.51%, and 1.12%, respectively, and the net NPA ratio was 1.35%, 1.64%, 2.20%, and 0.38%, respectively.

- Fusion Micro Finance Limited’s technology investments and initiatives over the years have yielded substantial increases in digital customer onboardings and online disbursements as well as a decrease in turnaround times. For the three months ended June 30, 2022, and the financial year 2022, all of our customers were onboarded digitally, and the share of cashless disbursements in total disbursements was 96.27% and 94.38%, respectively, while the average turnaround time for loan approvals decreased from approximately 13.2 days for the financial year 2016 to 5.1 days for the financial year 2022 and further to 3.9 days for the three months ended June 30, 2022.

Fusion Micro Finance Limited IPO Financial Performance:

Fusion Micro Finance Limited IPO Shareholding Pattern:

| Shareholding Pattern | Pre- Issue | Post Issue |

| Promoters & Promoters Group | 85.57% | 58.10% |

| Others | 14.43% | 41.90% |

Source: DRHP, EWL Research

Fusion Micro Finance Limited IPO Key Highlights:

-

Company’s revenue grew at a CAGR of 16.92% from Rs.720 Cr in FY20 to Rs.1151 Cr in FY22.

-

Profit after Tax decreased from Rs.69.61 Cr in FY20 to Rs.21.76 Cr in FY22 majorly due to increase in the impairment cost on the financial instruments.

-

Operating margin decreased to 4.7% in the last financial year from 19.7% in FY20.

-

The Gross GNPA of the company is at 3.67%, while Net NPA is at 1.35% as of June 30, 2022.

Fusion Micro Finance Limited IPO Risk Factors:

-

A large portion of FMFL’s collections and disbursements from customers are in cash, exposing it to certain operational risks, risk of theft and fraud.

-

Any downgrade of in credit ratings may adversely affect the cost of borrowings and results of operations.

-

The microfinance industry in India faces unique risks due to the category of borrowers that it services.

- A large portion of Fusion Micro Finance Limited’s collections and disbursements from customers are in cash, exposing it to certain operational risks, large cash collections, and disbursements expose it to the risk of theft, fraud, misappropriation, or unauthorized transactions by employees responsible for dealing with such cash collections. For the three months ended June 30, 2022, and the financial years 2022, 2021, and 2020, ₹72.38 crores, ₹339.28 crores, ₹372.93 crores, ₹1,594.64 crores, respectively, or 3.72%, 5.60%, 10.14%, and 44.63% respectively, of its loans were disbursed through cash. For the same periods, ₹1,526.90 crores, ₹4,648.24 crores, ₹3,254.05 crores, and ₹3,187.41 crores, respectively, of its collections were in cash.

- The microfinance industry in India faces unique kinds of risks due to the category of borrowers that it services, which are generally not associated with other forms of lending. The company’s focus customer segment is women in rural areas with an annual household income of up to ₹300,000. Customers generally have limited sources of income, savings, and credit histories.

- The Offer includes an Offer for Sale of up to 13,695,466 Equity Shares by the Promoters and certain other Selling Shareholders. The proceeds from the Offer for Sale will be transferred to the Selling Shareholders, which include the Promoters, pursuant to the Offer, who will have broad discretion over the use of such proceeds. The company will not receive any such proceeds from the Offer for Sale portion.

- Fusion Micro Finance Limited’s business and financial performance may be adversely affected in the event of any deterioration in the performance of any pool of receivables assigned or securitized to banks and other institutions or if any such assigned or securitized receivables are held to be unenforceable under applicable law.

Fusion Micro Finance Limited IPO Outlook:

FMFL is one of the youngest companies (in terms of getting an NBFC-MFI license) among the top NBFC-MFIs in India in terms of AUM as of June 30, 2022. The company has well-diversified and Extensive Pan-India Presence and it focuses to provide financial services to women entrepreneurs belonging to the economically and socially deprived section of the society. It majorly offers two products: Microfinance also called as microcredit and MSME. The company benefits from a large and diversified mix of 56 lenders comprising a range of public banks, private banks, foreign banks, and financial institutions, as of June 30, 2022. The company has generated strong revenue growth in the last 3 years however its margins are on a declining trend. At the higher end of the Price band, the IPO is priced at 170 times considering FY22 Earnings which is highly overpriced comparing to the average PE of its listed peers which is 106, so we recommend to avoid the IPO.

Fusion Micro Finance Limited IPO FAQ

Ans.Fusion Micro Finance Limited IPO will comprise fresh share issue and new offer share issue. The company aims to go public to accelerate its growth and expansion plan.

Ans. The Fusion Micro Finance IPO opens on Nov 2, 2022 and closes on Nov 4, 2022.

Ans. The minimum lot size that investors can subscribe to is 40 shares.

Ans. The Fusion Micro Finance IPO listing date is not yet announced. The tentative date of Fusion Micro Finance IPO listing is Nov 15, 2022.

Ans. The minimum lot size for this IPO is 40 shares.