TVS Motor Company is one of the leading global manufacturers of two & three-wheeler vehicles, driving innovation and progress in sustainable mobility. With state-of-the-art manufacturing facilities in Hosur, Mysuru, and Nalagarh in India, as well as Karawang in Indonesia, TVS is committed to producing high-quality, internationally aspirational products through innovative and sustainable processes. With a legacy of trust, value, and service spanning over 100 years, TVS has built a reputation for excellence. The company’s subsidiary, Norton Motorcycles, is a prestigious brand in the UK, while its e-mobility subsidiaries—Swiss E-Mobility Group (SEMG) and EGO Movement—are leaders in the e-bike market in Switzerland. TVS continues to deliver superior customer experiences across over 80 countries globally.

| Recommendation | Accumulation Price | Target Price | Time Horizon |

| Accumulate | Rs.2,375 – 2,400 | Rs. – 2,900 | 12 Months |

| Stock Details | |

| Market Cap. (Cr.) | 1,16,033 |

| Equity (Cr.) | 47.51 |

| Face Value | 1 |

| 52 Wk. high/low | 2958 / 1873 |

| BSE Code | 532343 |

| NSE Code | TVSMOTOR |

| Book Value (Rs) | 163.32 |

| Industry | Automobiles |

| P/E | 58.6 |

| Share Holding Pattern % | |

| Promoter | 50.27 |

| FIIs | 21.20 |

| Institutions | 19.99 |

| Public | 8.52 |

| Total | 100 |

Key Investment Rationale:

•EV & Future Products: TVS Motor’s EV segment is growing rapidly with the iQube leading the market, offering variants like 2.2 kWh, 3.4 kWh, and 5.1 kWh. The launch of the TVS King EV MAX, a three-wheeler with 179 km range, highlights its commitment to expanding EV offerings and capturing a larger market share.

•Strategic Partnerships: TVS Motor has partnered with Hyundai at the Bharat Mobility Global Expo to unveil micro-mobility concepts. This collaboration strengthens TVS’s position in the EV and micro-mobility segments, helping accelerate the development of innovative products and expanding its market presence.

•Export Market Expansion: TVS Motor continues to expand in Latin America, especially Brazil, focusing on brand-building, customer service, and spare parts availability. By establishing a strong distribution network, TVS aims to increase market share, particularly with the growing demand for EV products in this high-growth region.

•Investment in DriveX: TVS has increased its stake in DriveX, a used vehicle business, to strengthen its presence in India’s growing used vehicle market. This strategic investment enhances TVS Motor’s operations, creating synergies and building a robust platform to serve the expanding automotive sector in India.

•International Investment Strategy: TVS has strategically invested in global subsidiaries like Norton and TVS Singapore to expand its international presence. Additionally, investments in Dubai target the Middle Eastern, African, and European markets. The company focuses on technology, product development, and regional brand building to drive growth in these areas. This global expansion supports TVS’s long-term goals of diversifying revenue streams and strengthening its international footprint.

Indian Economy Overview

India’s economy is projected to grow at 6.5% in FY2025, driven by strong domestic demand, strategic government investments, and expansion across key sectors. The industrial sector has demonstrated resilience, with manufacturing and mining contributing positively to the Index of Industrial Production (IIP). The services sector, particularly trade, transport, and financial services, remains a key growth driver. Active fiscal and monetary policies from the Government and RBI have fostered this growth, with the RBI maintaining a consistent stance on lowering interest rates to support industrial expansion and stabilize the INR. Core inflation has moderated and is expected to ease further with normal monsoons anticipated in the coming fiscal year.

The government’s continued push for infrastructure development is evident, with public capital expenditure rising from ₹7.28 lakh crore in FY 2022-23 to ₹10 lakh crore in FY 2023-24, and an additional outlay of ₹11.1 lakh crore for FY 2024-25. This infrastructure build will enhance short-term economic vitality and long-term quality of life.

As India digitizes, financialization, formalization, urbanization, and premiumization will be significant growth drivers. Strong economic fundamentals, a young skilled workforce, rising discretionary consumption, and improved ease of doing business are transforming India into a prime destination for FDI. According to the IMF, India is projected to become the world’s third-largest economy by 2027.

Indian Automotive Industry Performance

The Indian automotive industry recorded a growth of 3.1% in Q3 FY25, as per the Society of Indian Automobile Manufacturers (SIAM) report, driven by the country’s macroeconomic stability, which fostered growth across various vehicle segments. During the period from April to December 2024, the industry grew by 9.2%, with significant contributions from the two-wheeler, three-wheeler, and passenger vehicle segments. However, the commercial vehicle segment faced a decline.

The passenger vehicle industry saw the highest YoY growth of 4.5% in Q3 FY25, with 1,058,145 units sold in 2024 compared to 1,012,285 units in 2023. The two-wheeler industry continued its strong performance, registering a 3% YoY growth, with 48,74,590 units sold, up from 47,31,436 units in Q3 FY24. The commercial vehicle segment showed modest growth of 1.2%, with 2,38,050 units sold, compared to 2,35,262 units in the same period last year. The three-wheeler segment posted marginal growth of 0.2%, with 1,88,853 units sold in Q3 FY25, slightly up from 1,88,434 units in Q3 FY24.

For the full fiscal year, the passenger vehicle industry grew by 1.8% YoY, with 31,39,288 units sold in FY25 compared to 30,83,245 units in FY24. In contrast, the commercial vehicle segment experienced a 2.3% YoY decline, with 6,83,471 units sold. The three-wheeler segment expanded by 6.4%, with 5,62,652 units sold, while the two-wheeler sector saw the highest growth of 11.6%, with 1,50,39,570 units sold in FY25 compared to 1,34,70,842 units in FY24.

Management Commentary on the business & its future prospects:

- Market Outlook: TVS Motor is optimistic for Q4, expecting strong rural market growth driven by better crop forecasts, infrastructure investments, and favourable weather. The company anticipates continued growth in both domestic and international markets, with rural trends and infrastructure development as key growth drivers.

- OBD2B and Price Hikes: The OBD2B phase change, effective from April 1, 2025, will introduce minimal price hikes. TVS anticipates slight price increases, similar to the 1.5%-2% observed during previous regulatory transitions, while preparing products for compliance.

- Gross Margin Stability: Despite a growing EV share, TVS Motor has maintained stable gross margins. This is due to effective product mix management, material cost reductions, and competitive pricing strategies, ensuring margin stability amid rising electric vehicle sales.

- Operating Leverage and Employee Costs: TVS has seen increased employee costs due to investments in new technologies and capacity building. These are considered strategic for future growth, especially in EVs, with expected returns in the next 2-3 years, though short-term costs will rise.

- PLI Benefits and Q4 Expectations: TVS expects to recognize Production-Linked Incentive (PLI) benefits in Q4 FY2025, with the iQube EV approved under the scheme. This will positively impact revenue and margins, with ongoing quarterly PLI recognition thereafter.

- Electric Two-Wheelers Growth: TVS has expanded its electric scooter network to nearly 900 dealerships. The iQube EV and traditional models like Jupiter and Ntorq aim to capture market share as the scooter market in India reaches 40% penetration.

- Rural Market Recovery: TVS is optimistic about continued growth in rural markets, now performing similarly to urban areas. Good monsoon conditions and favourable economic factors are expected to sustain growth into FY2025, although challenges persist in entry-level segments.

Q3FY25 Result Analysis

- Revenue Performance: In Q3FY25, the company reported a revenue from operations of INR 11,134.63 crore, reflecting a growth of 10.1% compared to INR 10,113.94 crore in Q3FY24 on a YoY basis. However, on a QoQ basis, the revenue declined by 1.47% from INR 11,301.68 crore in Q2FY25.

- Profit after tax: The Company reported a profit after tax (PAT) of INR 609.35 crore, marking a YoY increase of 19.6% from INR 509.61 crore in Q3FY24 and a 6% increase compared to INR 588.13 crore in Q2FY25.

- EBITDA Performance: For Q3FY25, the company’s EBITDA stood at INR 1,643.75 crore, showing an 11.4% growth from INR 1,475.21 crore in Q3FY24 on a YoY basis. On a QoQ basis, EBITDA grew marginally by 1.24% from INR 1,623.54 crore in Q2FY25.

- EBITDA Margin: The EBITDA margin improved to 14.76% in Q3FY25 from 14.59% in the same quarter last year, and from 14.37% in the preceding quarter, indicating strong operational efficiency.

- The Company recorded sale of 35.3 Lakh units, grew by 13% during the nine months period as against 31.3 Lakh units reported in the nine months period of last year

Profit and Loss Statement:

| Particulars (In Cr) | FY24 | FY23 | FY22 |

| REVENUE | |||

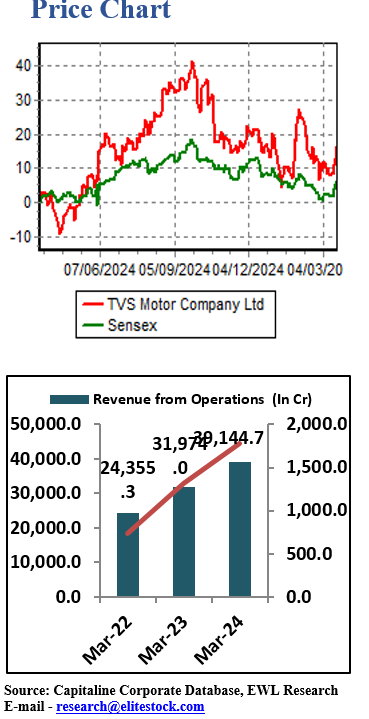

| Revenue From Operations | 39144.74 | 31973.99 | 24355.31 |

| Other Income | 105.82 | 138 | 32.87 |

| Total Revenue | 39250.56 | 32111.99 | 24388.18 |

| EXPENSES: | |||

| Cost of Materials Consumed | 23717.91 | 20096.24 | 15938.65 |

| Purchases of Stock-in-Trade | 1011.69 | 890.95 | 579.04 |

| Changes in Inventories of Finished Goods, WIP and SIT | -324.35 | -140.93 | -260.4 |

| Employee Benefits Expenses | 3385.19 | 2890.25 | 2124.62 |

| Finance Costs | 1927.72 | 1367.89 | 940.22 |

| Depreciation and Amortization Expenses | 975.12 | 858.86 | 742.86 |

| Other Expenses | 5810.89 | 4170.1 | 3218.77 |

| Total Expenses | 36504.17 | 30133.36 | 23283.76 |

| Profit before Exceptional and Extraordinary Items and Tax | 2702.92 | 1937.9 | 1106.91 |

| Exceptional Items | 0 | -1.87 | -40.12 |

| PBT | 2702.92 | 1936.03 | 1066.79 |

| Tax Expenses | 924.38 | 626.57 | 335.91 |

| PAT | 1778.54 | 1309.46 | 730.88 |

Balance Sheet:

| Particulars (In Cr) | FY24 | FY23 | FY22 |

| SOURCES OF FUNDS : | |||

| Share Capital | 47.51 | 47.51 | 47.51 |

| Reserves Total | 6736 | 5457.49 | 4351.94 |

| Total Shareholder’s Funds | 6783.51 | 5505 | 4399.45 |

| Minority Interest | 727.6 | 404.85 | 653.56 |

| Secured Loans | 22466.05 | 17029.99 | 11280.25 |

| Unsecured Loans | 3539.65 | 5345.59 | 4546.96 |

| Total Debt | 26005.7 | 22375.58 | 15827.21 |

| Other Liabilities | 301.68 | 268.4 | 250.97 |

| Total Liabilities | 33818.49 | 28553.83 | 21131.19 |

| APPLICATION OF FUNDS : | |||

| Gross Block | 11760.81 | 10819.8 | 10468.65 |

| Less: Accumulated Depreciation | 5869.99 | 5071.77 | 4494.01 |

| Net Block | 5890.82 | 5748.03 | 5974.64 |

| Capital Work in Progress | 1032.95 | 743.45 | 551.53 |

| Investments | 1123.19 | 967.25 | 604.56 |

| Current Assets, Loans & Advances | |||

| Inventories | 2248.4 | 1921.51 | 1642.36 |

| Sundry Debtors | 1839.42 | 1256.42 | 1177.3 |

| Cash and Bank | 2425.73 | 1879.11 | 1535.61 |

| Loans and Advances | 14843.27 | 11775.32 | 8402.13 |

| Total Current Assets | 21356.82 | 16832.36 | 12757.4 |

| Less : Current Liabilities and Provisions | |||

| Current Liabilities | 8004.29 | 6338.92 | 5680.49 |

| Provisions | 201.22 | 131.79 | 107.42 |

| Total Current Liabilities | 8205.51 | 6470.71 | 5787.91 |

| Net Current Assets | 13151.31 | 10361.65 | 6969.49 |

| Deferred Tax Assets | 584.95 | 466.04 | 359.15 |

| Deferred Tax Liability | 387.13 | 368.68 | 348.83 |

| Net Deferred Tax | 197.82 | 97.36 | 10.32 |

| Other Assets | 12422.4 | 10636.09 | 7020.65 |

| Total Assets | 33818.49 | 28553.83 | 21131.19 |

Cash Flow Statement:

| Particulars (In Cr) | FY24 | FY23 | FY22 |

| Cash and Cash Equivalents at Beginning of the year | 1851.19 | 1445.68 | 1573.76 |

| Net Cash from Operating Activities | -1252.67 | -4404.81 | -1575.19 |

| Net Cash Used in Investing Activities | -1001.36 | -1307.76 | -1470.91 |

| Net Cash Used in Financing Activities | 2758.64 | 6118.08 | 2918.02 |

| Net Inc/(Dec) in Cash and Cash Equivalent | 504.61 | 405.51 | -128.08 |

| Cash and Cash Equivalents at End of the year | 2355.8 | 1851.19 | 1445.68 |

Outlook:

TVS Motor is a leading manufacturer of Two & Three-wheeler vehicles, offering a diverse range of products with a strong global presence across regions such as the Middle East, Africa, Southeast Asia, the Indian subcontinent, and Latin & Central America. The company is actively expanding its market share in the electric vehicle (EV) Two-wheeler segment and also enhancing its product portfolio by introducing premium Two-wheeler bikes to meet evolving customer demands.

Over the past nine months, the company reported a revenue of Rs 32,843.17 crore, reflecting a 12% growth on YoY basis. And it reported a PAT of Rs 1,682.30 crore, marking a 23% growth YOY basis, and an EBITDA margin of 14.35%. The company also posted an EPS of Rs 33.41 and is currently trading at a TTM P/Ex of 58.6.

Given the company’s robust financial performance, strategic investments in subsidiaries, partnerships, the launch of electric vehicle (EV) products, and strong management guidance for margins and the outlook for Q4 FY25, we believe TVS Motor is well-positioned for continued growth.

Based on these factors and our expectations, We recommend that investors accumulate TVS Motor stock within the price range of Rs. 2,375–2,400, with a target price of Rs. 2,900 over the next 12 months.

Source: Company website, EWL Research

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India. (SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Vindhyachal Prasad, Elite Wealth Limited, vindhyachal@elitestock.com

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

- all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

- No part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or emailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale. Legal Entities Disclosures

Mr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone: 011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

- Reports

- a) EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

- EWL or its associates or relatives, have no actual/beneficial ownership of one %. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

- EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

- Compensation

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

- EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

- EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research

- In respect of Public Appearances

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL