Journey of Indian Stock Market in CY21 and Outlook for CY22

Rally of the Market

In Year 2021, Indian Stock Market was one of the best performing market in the world, Nifty gave return of 26% YTD this year while mid and small cap perform better than largecap. Within the large cap Index, IT was the outperformer with 54% return and Bank Nifty was an underperformer with 18% return. This rally in markets was on the back of very easy liquidity, strong earning recovery and very strong retail participation. This year Primary market was also very active as new age companies entered the market. Market was in a bull trend till October as every dip was very quickly bought into. From October onwards bulls are taking a breather, digesting this big gain and consolidated in a range.

From October onwards market faced few negative events like china Evergrande issue, rise in crude price, high inflation in India and world, new covid variant and Federal Reserve signaling early and fast QE tapering that impacting market. As market was at high valuation market needed a trigger for correction and finally it got it. Market has recently corrected 10% from its highs and now consolidating within a range. One of the biggest positive for this year was the DIIs participation which has constantly absorbed FII selling, this year FII has sold roughly 80000 crore. The biggest reason of their outflow from India is the premium valuation as most major Global brokerage firms from October onwards has been downgrading India, then the faster tapering of QE by US Fed and also raising interest rate forecast, FII are also selling in secondary market to participate in primary market.

Outlook for 2022

Going forward, We feel next year market to consolidate in the first Quarter of the CY. However as the earning catch up valuation corrects itself so we can expect renewed participation from the market participants due to better earnings and better valuations. Biggest trigger for next year is going to be US Fed Tightening Policy, Inflation around the world, State Election in five state, market will be keenly watching the UP election verdict as it is the biggest state of India, corporate earning and RBI stance on Interest Rate . So for the long term prospectus Investor should look any significant dip as an opportunity to buy for long term , as earning cycle is finally showing sign of bottoming out, credit cycle is expected to pick up, IT sector is seeing very strong demand and realty sector is making a come back after a decade. India looks in a sweet spot but turbulence in between will continue and Investor should make full use of those dips.

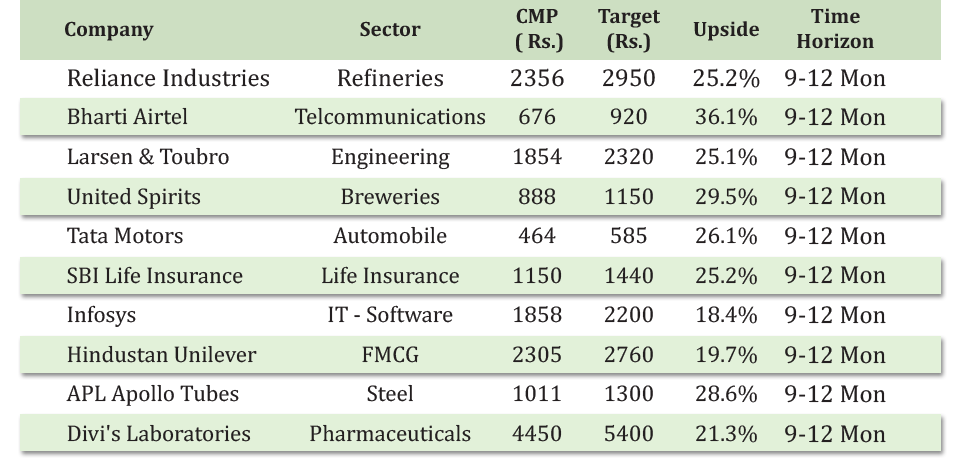

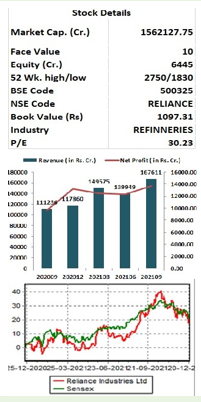

Reliance Industries Ltd.(CMP –Rs.2356 Target – Rs.2950)

Reliance Industries is one of India’s biggest conglomerates with a presence in oil refining & petrochemicals, oil & gas exploration, retail, digital services and media, etc,. On a consolidated basis, Majority of revenue come from oil and gas segment, while retail contribute 28%. At the EBITDA level, O2C and oil & gas contributed 43% while retail, digital and others contributed 11%, 38% and 8%, respectively.

Key Takeaways:

- Reliance Jio, the telecom vertical of Reliance Industries have taken a 20% tariff hike, which is going to improve ARPU of the company. Further, improving traction in JioPhone Next should be an aiding factor. The company is keen to target a large chunk of the 300 million Feature Phone market through JioPhone Next.

- RIL, in the last year, has seen strong deleveraging on the back of value unlocking in the Consumer business, and they have raised capital through right issue.

- Reliance GRM has fallen in the first half of FY21, However, the Petrochem segment should offset the impact on the back of good demand and continued delays in upcoming capacities.The Digital business, over the last couple of years, has seen a strong ramp-up, partly . It has reached 20% of core retail revenues, Key operating metrics such as daily orders, average order values, delivery timelines, and order returns have all been improving significantly. The key factors supporting JioMart are the physical store connectivity and new warehouses, which have ramped up the supply chain.

Outlook:

Being one of the two leading players in telecom space, Airtel is capitalizing on every opportunity. Factors such as work from home, streaming of more entertainment content online, and home schooling continue to boost the performance of the company. With the recent tariff hike, ARPU expected to increase for the industry and Bharti with the highest ARPU in the industry is set to benefit from this move which is expected to increase earnings of the company by 20-25% in next 2 years as per our estimates. Hence, investors can buy the stock at CMP of Rs. 676 at the current level for target price of Rs.920. Time frame should be 9-12months.

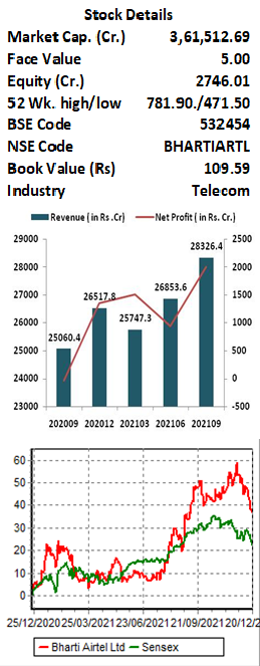

Bharti Airtel Ltd. CMP – Rs. 676 Target – Rs.920

Bharti Airtel is a leading global telecommunications company with operations in 18 countries across Asia & Africa. Airtel’s portfolio includes high speed 4G mobile broadband, Airtel Xstream Fiber, converged digital TV solutions through the Airtel Xstream 4K Hybrid Box, digital payments through Airtel Payments Bank as well as an integrated suite of services across connectivity, collaboration, cloud & security.

Key Takeaways:

- APRU to increase with Tariff Hike: Airtel is gradually increasing tariff with the aim to reach ARPU of Rs. 200 by FY22 end and Rs. 300 over the long term.

- 5G to come in FY23: The 5G auctions are likely to happen in July 2022 instead of May as Telecom Regulatory Authority of India (TRAI) likely to submit its pricing recommendations to the Department of Telecommunications (DoT) only in March and it will take six months to start offering 5G services from when the spectrum is allotted. However Airtel conducts India’s first Rural 5G trial in partnership with Ericsson and also collaborated with Capgemini to bring 5G-based enterprise grade solutions to the India.

- Targeting 2x Net Debt/ EBITDA: It will be comfortable with net debt to EBITDA of 2x and aims to achieve this. It has a monetization opportunity, through Africa, Indus, etc. and increasing cash flow from growth in the existing business.

- Investment in UK based space start-up OneWeb: OneWeb is planning to launch fleet of 648 Low Earth Orbit Satellites that will deliver high-speed, low –latency global connectivity globally by May 2022 including in India.

Outlook:

Being one of the two leading players in telecom space, Airtel is capitalizing on every opportunity. Factors such as work from home, streaming of more entertainment content online, and home schooling continue to boost the performance of the company. With the recent tariff hike, ARPU expected to increase for the industry and Bharti with the highest ARPU in the industry is set to benefit from this move which is expected to increase earnings of the company by 20-25% in next 2 years as per our estimates. Hence, investors can buy the stock at CMP of Rs. 676 at the current level for target price of Rs.920. Time frame should be 9-12months.

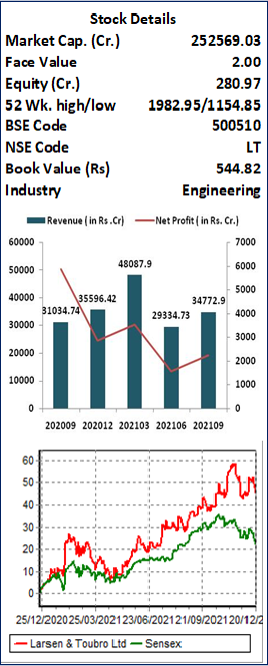

Larsen & Toubro Ltd. CMP – Rs. 1854 Target – Rs. 2320

Larsen and Toubro (L&T) is major engineering, construction, manufacturing, technology, and financial services conglomerate, with global operations. L&T addresses critical needs in key sectors – Hydrocarbon, Infrastructure, Power, Process Industries and Defence – for customers in over 30 countries around the world.

Key Takeaways:

- L&T’s order inflow grew by 13 per cent YoY to Rs 26,600 crore in the June quarter with total Order book stood at Rs. 3.23 trillion, comprising of Infrastructure (76%) and Hydrocarbon (13%) orders. Management guided low to mid double-digit growth in the order book inflows for FY22. As central and state governments, which typically account for 40 per cent of the order book, push on to utilize the expenditure portion of the budget, order flow is likely to improve in H2FY22.

- Company’s second largest revenue contributor and largest EBIT contributor segment technology services is growing in double digits through LTI, LTTS and Mindtree reflecting a surge in demand for technology led offerings.

- The company Kept its guidance of low to mid double-digit growth for sales in FY22 and confident to maintain its core margins at the same level as last year despite increasing commodity costs.

Outlook:

Larsen & Toubro has a well-established track record in the infrastructure segment. Company’s focus continues to be on efficient execution of its large order book, working capital reduction, cost optimization through use of digital technologies aimed at operational efficiencies. Working capital of the company remains under control, despite a mild seasonal deterioration at the group level, the objective is to reduce the debt level sequentially. The union government has increased the capital expenditure by 34% to Rs 5.5 lakh crore for FY22 in Budget which would benefit the company to improve order book. On performance front we expect company to report EPS of Rs.92.1 for FY23E, at CMP of Rs.1854 PE works out to be 19.8x. Hence, investors can buy the stock at CMP of Rs.1854 for target price of Rs.2320. Time frame should be 9-12months.

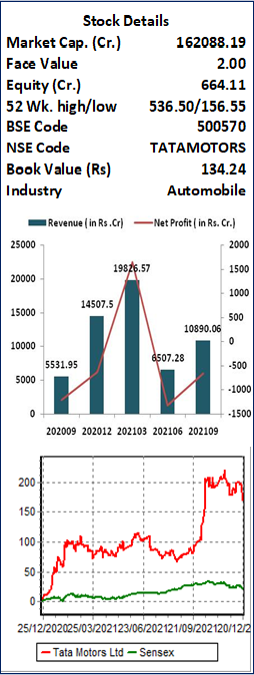

Tata Motors Ltd. CMP – Rs. 464 Target – Rs.585

Tata Motors Limited (TML) is a leading global automobile manufacturing company. Its diversified portfolio includes an extensive range of cars, sports utility vehicles, trucks, buses and defence vehicles. Jaguar Land Rover (JLR), part of Tata Motors since 2008, is Britain’s largest automotive manufacturer which designs, manufactures and sells some of the world’s best-known premium cars such as Jaguar and Land Rover.

Key Takeaways:

- TATA Motors has establishing itself as a leader in Indian EV market .It’s Product range in EV includes Nexon, Tigor and X-Press T with 75% Market Share in EV four wheeler Market. In eight months of FY22 Tata Motors registered 272% YoY growth with cumulative EV sales of 7,756 Units.

- EV penetration in India is well poised to witness sharp penetration and Tata Motors will plan for 20% penetration in 5 years by launching one or two product every year. Worldwide, JLR has announced a Reimagine strategy of converting the entire Jaguar portfolio into an electric-only portfolio starting FY 24.

- Tata UniEVerse – a Tata Group consortium committed to address the e-mobility ecosystem Group companies working in Sync with TATA Motors to develop the EV Ecosystem in India: TATA CHEMICALS(Lithium Ion Cell manufacturing and Recycling).TATA AUTOCOMP(Battery Manufacturing),TATA POWER (Charging Infrastructure),TATA MOTOR FINANCE(Finance Facility to adopt EVs).

- Tata Motors Tigor is qualified for FAME and is witnessing very steep increase in demand in the states where incentives are being extended.

Outlook:

Tata Motors is betting big on EV Market and targets cash and EBIT margin positive in H2FY22. The Auto Industry is facing the semiconductor shortage with Tata Motors Production is too impacting however it continues to priorities production of higher margin and less chip dependent products while working on reducing dependence on chips. The situation is expected to ease in a gradual manner. In PV Segment. The company launched one model Tata Punch micro-SUV which is seeing strong demand. Hence, investors can buy the stock at CMP of Rs.464 for target price of Rs.585. Time frame should be 9-12months.

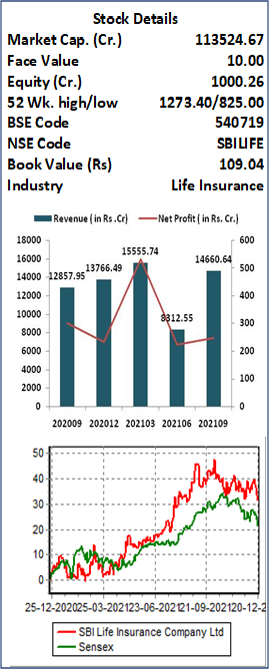

SBI Life Insurance Company Ltd. CMP – Rs. 1150 Target – Rs.1440

SBI Life Insurance is a joint venture between State Bank of India and BNP Paribas. It holds Private market leadership in Total New Business Premium (NBP) with 22.6% market share and have cost leadership in Industry with lowest expense ratio of 9.5%. It Has strong solvency ratio of 2.12

Key Takeaways:

- SBI Life top the Total APE growth ( Annualized Premium Equivalent) in YTD FY22 with 39% YoY Growth. In November month of 2021 SBI Life registered strong growth of 48% YoY in APE. In NBP ( New Buisness Premium) too SBI Life witnessed exceptional growth of 150 per cent YoY in November month against the growth of 58.63% YoY of whole Private Insurers’ NBP.

- New Business premium registered growth of 77% in H1FY22. Persistency Ratio of SBI Life improved from 83.2% in H1FY21 to 84.7% in H1FY22 due to focus on improving the quality of business and customer retention. Value of New Business Margin too improved by 510 bps to 25.3% in H1FY22.

- In First half of Fiscal 2021 SBI Life received a total of 22,606 claims Net of reinsurance, claim amount stood at Rs 1,340 crore. Of these, 8,956 claims pertain to the first quarter. So, total claims received in the second quarter stood at 13,650, that is 1.5 times the claims in the first three months.

Outlook:

SBI Life insurance is the leading private Insurance company. For FY22, the management of the SBI Life expects the share of non-par at 12-13% in their Product Portfolio. Over the medium-to-long term, the non-par share may increase to 15-18%. The shift in product mix towards higher margin products such as non-par would help in improvement of VNB margin of the company. SBI Life has set aside an additional reserve of Rs 266 crore towards Covid-19 pandemic as of September 2021. Hence, investors can buy the stock at CMP of Rs.1150 for target price of Rs.1440. Time frame should be 9-12months.

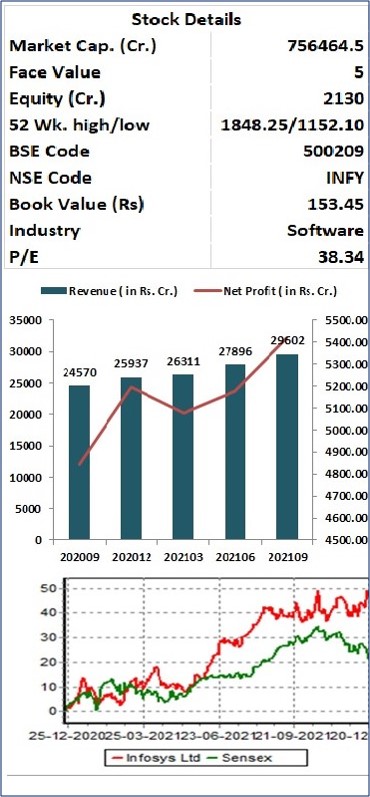

Infosys Ltd. CMP – Rs.1858 Target – Rs.2200

Infosys Limited is one of the oldest and largest providers of IT consulting and software services, including E-business, program management and supply chain solutions. Infosys services include application development, product co-development, and system implementation and system engineering. Infosys targets businesses specializing in the insurance, banking, telecom and manufacturing sectors. Company has 260,000 employees and highest revenue come from United states.

Key Takeaways:

- For FY22 Company has guided for the revenue growth of 16.5% – 17.5% in constant currency terms, and operating margin guidance at 22%-24%.

- Around 32% of the revenue come from BFSI segment which saw a growth of 21.53% in Q2FY22.Manufacturing sector saw growth of 43% Y-o-Y.

- Company won 22 large deals of over $50mn in Q2FY22, totaling $2.15bn TCV. Regionally, 15 were from Americas, 6 from Europe and 1 from Rest of the World. The share of the new deals in Q2FY22 was 37%.

- In FY21 Company generated cash flow of 3.3 Billion dollar and free cash flow of 3 Billion dollar. In FY21 they did a buy-back of ₹ 11093 crore.

OUTLOOK:

Infosys is the second largest IT consultancy company of the country. In FY21, around 41% of the revenue come from digital segment which is high margin segment for the company. North America Saw a growth of 23% in the second quarter of FY22 which is the largest market for the company. After second quarter company has increased their revenue guidance to 17%.In FY22 United states technology spending is expected to reach 2.075 trillion dollar and Infosys being a large player in US is expected to do well. Infosys is a cash generating machine produces around $3 Billion of cash flow which is used by the company in paying dividend and doing buyback. As organizations around the world have increasing their digital spending, which will give benefit to Indian companies and Infosys being a large player with great reputation among its client is going to be benefitted by this IT boom. We recommend buying Infosys at current market price for the target of Rs. 2200, as Infy is well-placed for growth from a long-term perspective backed by multiple long-term contracts with the world’s leading companies.

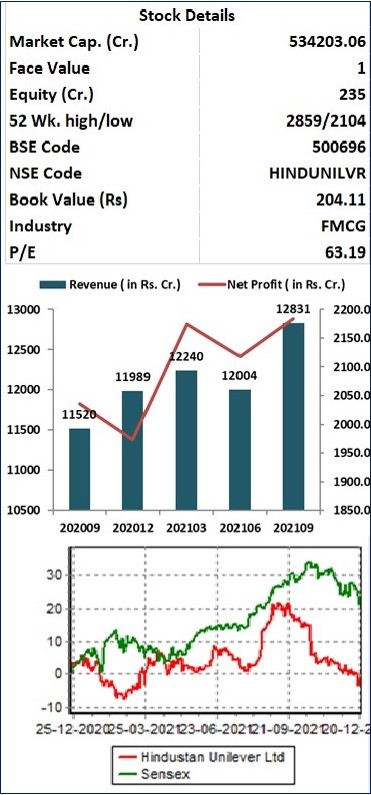

Hindustan Unilever Ltd. CMP – Rs. 2287 Target – Rs. 2760

HUL is India’s largest fast-moving consumer goods company with well-renowned household products. With 44 brands spanning 14 distinct categories such as soaps, detergents, shampoos, skin care, toothpaste, deodorants, cosmetics, tea, coffee, packaged foods, ice cream, and water purifiers, Hindustan Unilever (HUL), a subsidiary of Unilever PLC, has a very strong brand presence and is a market leader in majority of the products they deals in.

Key Takeaways:

- HUL continued to gain market share in 75% of their business, Beauty and Personal care is their Biggest segment in terms of revenue and also contribute highest margin.

- In second Quarter company reported 4% volume growth, while total revenue growth came at 11%.Company recently has taken price hike to offset raw material cost.

- HUL is the market leader wit very strong brand value so any cost pressure has always been passed on to the customer to maintain their margin.

- Company is having strong focus on digital space and now 15% of the total revenue come from this space.

- It has a very strong innovating pipeline and they are preparing to launch new products in coming quarter which will be margin accretive.

Outlook:

HUL is a subsidiary of unilever PLCn, its products are spread across discretionary and non-discretionary segments comprising of health, hygiene and nutrition products. HUL strengthened its market leadership despite inflationary headwinds. Nutrition business is expected to post healthy growth as business returned to normalcy post supply chain disruption and also improved in-mobility and improving out-of-home consumption. Company has taken price increases to offset raw material inflation hence the impact on persistent inflation on margins could be limited and company would be able to maintain the guided margin band of 24-25% for FY22.Company has the right growth matrix like a broad-based portfolio, continued cost savings agenda, growing traction in GSK business, and execution power. Given the volatile market outlook and relatively stable earnings growth trajectory we believe HUL could perform well. At CMP of Rs.2287 we are recommend buy for the target of Rs.2760 with time horizon of next 9-12 months

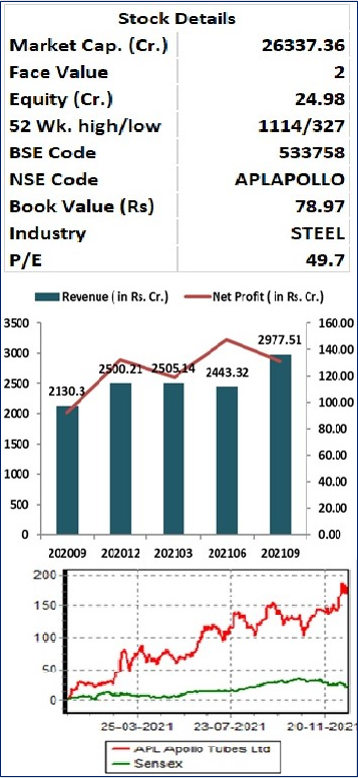

APL Apollo tubes Ltd. CMP – Rs.1011 Target Rs. 1300

APL Apollo Tubes is one of India’s leading manufacturers of branded steel products. Company has multi-product offerings include over 1100 varieties of MS Black pipes Galvanized Tubes, Pre-Galvanized Tubes, Structural ERW Steel tubes and Hollow Sections. The Company serves a wide spectrum of steel structural products catering to an array of industrial applications such as urban infrastructure, automobile, construction, housing, energy, irrigation, solar plants. greenhouses and engineering. It has 10 manufacturing Plant with total capacity of 2.55 MPTA.

Key Takeaways:

- APL is the market leader in structural Tube market in India with the market share of 50%, they have a pan India presence with 800 dealers and has constantly increased its capacity.

- APL Apollo was the first domestic player to introduce Direct Forming Technology (DFT) in India, an Italian technology used for tube manufacturing. With the introduction of DFT, company is able to manufacture tubes tailor-made to client requirements, which require less lead time and are cost effective also.

- The company is able to manufacture large jumbo tubes, which is not possible under old methods. Market is transiting to structural tubes, recently the Delhi government announced construction of seven hospital building using 100% structural steel tubes and the company is the sole supplier.

Outlook:

APL currently dominates the structural tubes market with 50% share, it is best placed to benefit from the growing Structural Steel Tubes industry as it has first mover advantage and strong brand name. It is expected that realty sector is making a comeback after a decade which will boost revenue for this company as customer are shifting from conventional tubes to structural tubes. Company has taken Several cost-control measures and with the increase in volume operating leverage will also kick in which will lead to improved margin and higher cash generation. Company recently changed their credit policy which has reduce its net working capital and has also reduce their debt quiet significantly. At CMP of Rs.1011 we recommend buy the stock for the target price of Rs.1300 with time horizon of next 9-12 months

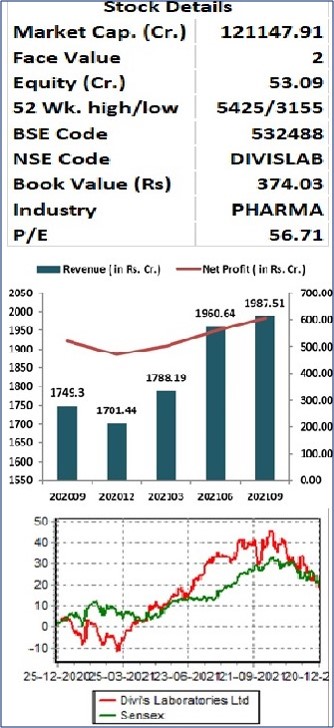

Divi’s laboratories Ltd. CMP – Rs.4450 Target – Rs. 5400

Divi’s laboratories headquarterd in Hyderabad is the second largest Pharma company in terms of market cap in India. The company is engaged in manufacture of leading generic compounds such as Nutraceutical ingredients and custom synthesis of APIs and intermediates for global innovator companies. Company has a portfolio of 120 products across diverse therapeutic areas. The company has four manufacturing facilities and market presence across several countries

Key Takeaways:

- In FY21, Europe was the largest market of the company as it contributed 47% of the revenue, then it is North America with 23% sale. Exports accounted for 88% of sales.

- It has built long-lasting relationships with innovators and have partnership with six of the top 10 Pharma innovators. The recent supply contract for Molnupiravir API with Merck/MSD shows that Divi’s is a partner of choice for critical projects for global innovators

- Divis has pipeline of 16 molecules which are under various stages of development, which is going to drive revenue in coming years.

- Divi’s future growth is going to be driven primarily by custom synthesis business while generics and strong positioning of Divis will help in monetising the growth opportunity in API and CRAMS space given its stellar execution track record, recent capex of Rs 2000 crore and being one of the preferred suppliers.

Outlook:

Divi’s is India’s largest API player with a very strong chemistry skills, process skills, manufacturing scale from clinical to commercial qualities, and project execution. They are preferred partner for leading Pharma Companies in the world for custom synthesis . We expect solid CAGR over FY23, led by increased business prospects from CS and Generics, benefits from Molnupiravir supply to the innovator, improved growth in Nutraceuticals, new product additions in the Generics segment, as well as margin expansion on process and productivity improvements. At current Market price of Rs. 4450 it trade trade at 44x price to Earning on FY23 Earning which is below its long term averages. We recommend buying Divis at current market price for the target of Rs. 5400. Time frame should be 9-12months.

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India.( SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Israil Khan, Elite Wealth Limited, suhail@elitewealth.in

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

(1) all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

(2) no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the report.

For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or emailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale.

Legal Entities Disclosures

Mr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone:011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

1. Reports

a) EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

(b) EWL or its associates or relatives, have no actual/beneficial ownership of one per cent. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

(c) EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

2. Compensation

(a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

(b) EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

(c) EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(d) EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(e) EWL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research report.

3 In respect of Public Appearances

(a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

(b) The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL