| Recommendation | PRICE RANGE | Target Price | Time Horizon |

| Buy | ₹ 531 | Rs. 670 | 12 Months |

Stock Details |

|

| Market Cap. (Cr.) | 2328.68 |

| Equity (Cr.) | 45.13 |

| Face Value | 10 |

| 52 Wk. high/low | 612 / 502 |

| BSE Code | 543689 |

| NSE Code | UNIPARTS |

| Book Value (Rs) | 151.94 |

| Industry | Auto Ancillaries |

| P/E | 11.36 |

Share Holding Pattern % |

|

Promoter |

65.79 |

| FIIs | 7.69 |

| Institutions | 9.26 |

| Non Promoter Corp. | 1.42 |

| Public & Others | 15.84 |

| Government | 0.00 |

| Total | 100.00 |

Price Chart

Uniparts India Limited (UIL) is a global leader in supplying critical component and systems for the Off-Highway market in the Agriculture, Construction, Forestry and Mining (CFM) sectors. It is engaged into manufacturing, sales and export of linkage parts and components for Off – Highway Vehicles (OHVs) and serves globally to more than 25 countries.

Key Investment Rationale:

•UIL’s two core product verticals, three-point linkage for the agricultural tractors and precision machine parts, which is basically articulation joints for the construction machinery have significant market share globally and are poised to grow due to expected resilient demand of OHV end user.

•It is well placed to benefit from strong infrastructure spending, solid consumption and proposed PLI scheme in the Automotive and Auto components sectors.

•The company has become an integral part of the global and local supply chains of some of their key customers and has built a long standing relationship with world’s leading global farm & construction and forestry & mining equipment manufacturers across geographies.

•Company has in-house value engineering and process innovation capabilities, supported by product development programs undertaken jointly with some of their key customers which makes it different from other auto component suppliers.

•Global farming sector profits were highest in FY22 since 5 decades; this will increase the requirement of high value agriculture equipments and will aid the equipment replacements.

•US, major contributor in the UIL’s Revenue, has $1 trillion infrastructure plan, which will boost the demand for construction equipment as the country aims to modernize aging infrastructure assets.

•China+1 strategy: India is emerging as a viable alternative destination for reducing the reliance on manufacturing in China. This is creating better opportunities for companies like UIL.

•Healthy Financial position with improving financial and operating metrics. Company has shown 18% YoY growth in the revenue from operations and 29% YoY growth for the 9MFY23. UIL’s Ebitda margin and Pat margin is continuously growing and is at 23.4% and 15.2% respectively for the 9MFY23.

Business Overview:

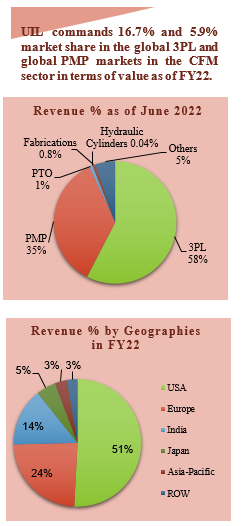

Unipart’s core product portfolio comprises 3-Point linkage systems and Precision machined parts. Company also manufactures adjacent product verticals that include Hydraulic cylinders, Power take off and Fabrications.3-Point Linkage Systems (3PL): The 3-PL system consists of different assemblies that are attached to an agricultural tractor. These systems are engineered and customized to each tractor model and are subject to validation and have to comply with international standards.Precision Machined Parts (PMP): PMP is a group of products that are components that require stringent material and manufacturing specifications and controls. These include among others, precision machined components such as pins, bushes and bosses used in articulated joints of construction, forestry and mining equipments. PMP products lack standardization due to the complex design and high degree of required precision.

Hydraulic Cylinders: These are used as actuators to move mechanized components by generating linear motion along an axis and are used in OHVs.

Power Take Off (PTO): PTO is a device used to drive implements such as rotary tillers, mowers and other equipment requiring a mechanical drive by the tractor. Uniparts is currently focused on producing PTO for the agriculture sector, which allows the transfer of power from the tractor to the implement.

Fabrications: Fabrications are used in agriculture as well as in construction equipment ranging from large structural parts and chassis to small and medium in size with no chassis parts. These parts vary in terms of size as well as design specifications and manufacturing process complexity.

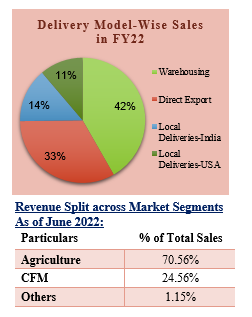

UIL’s Global Business Model:

Company serves OHV players including OEMs and aftermarket retail store chains, through its global business model.

International Sales: Sales in the Region outside India

Local Deliveries: Sales from manufacturing facility in India and United States, in their respective domestic markets

Direct Export: Export sales from Indian locations directly to overseas customers–

Warehouse Sales: Sales from warehousing facilities in their respective domestic markets

Manufacturing, Warehousing and Distribution Facilities:

| Manufacturing Facilities | 5 in India | 1 in US |

| Warehouses | 2 in US | 1 in Europe |

| Distribution Facility | 1 in India | – |

3PL Market – World Market for 3PL was USD 360-370 million in 2021 and is expected to grow at 6-8% between 2021 and 2026 encouraged by robust growth in tractor production volumes in North America, India, and Europe. A major driver of 3PL demand is tractors and the demand for 3PL is set to grow at a steady pace supported by:

- Growth in the global tractor production

- High level of farm mechanization and labour shortage

- Focus on innovation and new technologies

- Upgradation to higher Horse Power (HP) tractors by farmers

PMP Market – Global PMP market was USD 648 million in 2021, with more than 80% demand from four key geographies China, Japan, Europe, and North America. The demand for PMP products is expected to grow at a healthy CAGR of 6% – 8% between 2021 and 2026, supported by strong volume growth in construction equipment production in key markets such as the USA, Japan, and Europe. India will also contribute to this growth led by increased infrastructure projects.

Key Triggers/Highlights:

Leading presence in Global Off-Highway Market

UIL operates in more than 25 countries worldwide and is a well-known supplier of engineered systems and components to the Off-Highway market. As of FY22, it commands 16.7% market share in the global 3PL segment and 5.9% market share in the global PMP segment in terms of value in the Construction, Forestry and Mining segments.

Engineering driven, vertically integrated precision solution provider

The company has evolved from a component supplier to a provider of complete assemblies of precision engineered products which allow the company to offer integrated system solutions to meet its customer requirements and move up the value chain.

Long-term relationship with key global customers including OEMs

Company’s key global customers includes Tractors and Farm Equipment Limited (“TAFE”), Doosan Bobcat North America (“Bobcat”), Claas Agricultural Machinery Private Limited (“Claas Tractors”), Yanmar Global Expert Co. Ltd (“Yanmar”) and LS Mtron Limited among others. Four of company’s top five customers (based on revenue contribution during FY21) have been its customers for over 10 years. TAFE and Kramp are some of the customers with whom company has relationships for over 15 years. In the farm machinery or tractor space, UIL count all top 10 players as its customers while in the CFM domain, it counts 5 out of top 10 players at its customers. Its key customers in the farm machinery space in the domestic market include Mahindra & Mahindra, International Tractors (ITL), TAFE, Kubota-Escorts among others.

Focus on higher value addition products and Margin improvement

Company intend to continue to increase the margin accretive warehousing sales among other sales model mix and also intend to further expand its product portfolio with solutions for adjacent vehicle and equipment types such as utility task vehicles and all-terrain vehicles as well as focus on PMP products with a technology focus, such as, plungers and transmission components.

Consolidated Financials:

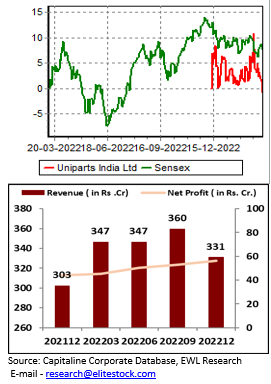

Quarterly Performance:

| Particulars (In Rs. Cr.) | Q3FY23 | Q2FY23 | Q3FY22 | QoQ% | YoY% | 9MFY23 | 9MFY22 | FY22 |

| Revenue from Operations | 331.18 | 359.76 | 302.52 | -7.9% | 9.5% | 1,037.79 | 880.89 | 1,227.42 |

| Other Income | 6.64 | 1.82 | 2.29 | 264.9% | 189.7% | 9.38 | 3.30 | 3.62 |

| Total Income | 337.82 | 361.58 | 304.82 | -6.6% | 10.8% | 1,047.16 | 884.19 | 1,231.04 |

| Cost of materials consumed | 114.70 | 137.20 | 135.70 | -16.4% | -15.5% | 391.71 | 386.22 | 501.26 |

| Changes in inventories | -0.43 | -12.90 | -47.74 | -96.7% | -99.1% | -29.79 | -112.12 | -99.70 |

| Employee expense | 60.45 | 59.79 | 54.44 | 1.1% | 11.0% | 178.97 | 160.59 | 219.69 |

| Other Expense | 77.58 | 96.04 | 93.29 | -19.2% | -16.8% | 263.18 | 248.15 | 338.13 |

| EBITDA | 78.89 | 79.63 | 66.83 | -0.9% | 18.0% | 233.71 | 198.05 | 268.05 |

| EBITDA Margin (%) | 23.8% | 22.1% | 22.1% | 170 bps | 170 bps | 22.5% | 22.5% | 21.8% |

| Finance Cost | 1.64 | 1.76 | 1.45 | -6.7% | 13.5% | 4.75 | 4.23 | 5.70 |

| Depreciation & Amortization expense | 10.09 | 9.87 | 9.18 | 2.2% | 9.9% | 29.55 | 27.17 | 36.65 |

| Profit Before Tax | 73.80 | 69.82 | 58.50 | 5.7% | 26.1% | 208.80 | 169.95 | 229.32 |

| Tax | 17.49 | 17.06 | 15 | 2.5% | 19.9% | 49.22 | 46.49 | 60.54 |

| Profit After Tax | 56.31 | 52.76 | 43.92 | 6.7% | 28.2% | 159.58 | 123.47 | 168.78 |

| PAT Margin (%) | 17.0% | 14.7% | 14.5% | 230 bps | 250 bps | 15.4% | 14.0% | 13.8% |

| EPS (in Rs.) | 12.71 | 11.94 | 9.88 | 6.4% | 28.6% | 36.07 | 27.99 | 38.17 |

Extract of Q2FY23 Earnings:

-

UIL generated highest ever revenue from operations of Rs.1037 cr. and Profit after Tax of Rs.159 cr. in the first nine months of FY23.

-

Company also generated highest ever Cash flow from Operations of Rs.144 cr. in the first nine months of the FY23.

-

Revenue from Operations of the company grew by more than 10% YoY in the Q3FY23 and 17.8% YoY for the 9MFY23; while Net Profits grew by 28% YoY in the Q3FY23 and 29% YoY for 9MFY23.

-

Company’s operating profits grew by 18% YoY in the quarter led by significant decrease in the material cost. EBITDA margin of the company improved sequentially as well as yearly by 170 bps and stands at 23.8% in the quarter.

-

Commenting on the latest results, management said that company’s commitment to its customers has only grown stronger over the years, and is continuously expanding its client base and product offerings in order to be the partner of choice for the valued customers. Management also believe the company is well set for exciting future ahead with engineering and design capabilities and Leading market presence in the off-highway systems segment.

Profit and Loss Statement:

| Particulars (In Rs. Cr.) | FY20 | FY21 | FY22 |

| Revenue from Operations | 907.20 | 903.10 | 1,227.40 |

| Other Income | 31.60 | 44.50 | 3.60 |

| Total Income | 938.80 | 947.60 | 1,231.00 |

| Cost of materials consumed | 332.30 | 338.20 | 501.30 |

| Changes in inventories | -3.50 | 14.70 | -99.70 |

| Employee expense | 211.80 | 185.40 | 219.70 |

| Other Expense | 270.50 | 245.40 | 338.10 |

| EBITDA | 127.7 | 163.9 | 271.6 |

| EBITDA Margin (%) | 14.1% | 18.1% | 22.1% |

| Finance Cost | 18.00 | 8.10 | 5.70 |

| Depreciation & Amortization expense | 35.40 | 37.30 | 36.60 |

| Profit Before Tax | 74.30 | 118.50 | 229.30 |

| Tax | 11.60 | 27.30 | 61 |

| Profit After Tax | 62.70 | 91.20 | 168.80 |

| PAT Margin (%) | 6.9% | 10.1% | 13.8% |

| EPS (in Rs.) | 14.00 | 21.00 | 38.00 |

Balance Sheet:

| Particulars (In Rs. Cr.) | FY20 | FY21 | FY22 |

| Equity and Liabilities | |||

| Equity | |||

| Equity Share Capital | 44.62 | 44.62 | 44.62 |

| Other Equity | 419.55 | 515.52 | 640.62 |

| Total Equity | 464.17 | 560.14 | 685.24 |

| Liabilities | |||

| Non-Current Liabilities | |||

| Borrowings | 21.61 | 5.72 | 4.86 |

| Lease Liabilities | 34.66 | 27.86 | 23.41 |

| Provisions | 13.83 | 15.61 | 16.73 |

| Deferred Tax Liabilities (Net) | 24.15 | 27.56 | 24.79 |

| Other Non-Current Liabilities | 0.88 | 0.93 | 1.02 |

| Total Non-Current Liabilities | 95.13 | 77.67 | 70.81 |

| Current Liabilities | |||

| Borrowings | 234.89 | 122.06 | 122.41 |

| Lease Liabilities | 7.24 | 6.53 | 7.24 |

| Trade Payables | 52.68 | 90.09 | 89.58 |

| Other Liabilities | 37.56 | 27.08 | 33.66 |

| Provisions | 6.31 | 5.47 | 5.47 |

| Current Tax Payable | 0.78 | 4.22 | 16.76 |

| Total Current Liabilities | 339.45 | 255.46 | 275.13 |

| Total Liabilities | 434.58 | 333.13 | 345.95 |

| Total Equity and Liabilities | 898.75 | 893.27 | 1,031.18 |

| Assets | |||

| Non-Current Assets | |||

| Property, plant and equipment | 207.00 | 200.19 | 206.22 |

| Right of use assets | 66.24 | 57.80 | 53.18 |

| Capital work-in-progress | 9.32 | 2.29 | 2.20 |

| Goodwill | 59.79 | 59.00 | 61.79 |

| Other intangible assets | 6.83 | 5.42 | 3.52 |

| Intangible assets under development | 0.63 | – | – |

| Other financial assets | 5.05 | 4.45 | 4.71 |

| Current tax assets (Net) | 11.23 | 11.28 | 14.84 |

| Other non-current assets | 0.45 | 2.23 | 2.61 |

| Total non-current assets | 367 | 343 | 349 |

| Current Assets | |||

| Inventories | 352.92 | 339.08 | 441.95 |

| Investments | – | 1.25 | – |

| Trade receivables | 122.84 | 167.53 | 194.23 |

| Cash and cash equivalents | 16.92 | 10.82 | 14.00 |

| Other balances with banks | 0.04 | – | – |

| Other financial assets | 0.17 | 3.90 | 3.90 |

| Other current assets | 39.32 | 28.01 | 28.00 |

| Total current assets | 532.19 | 550.59 | 682.07 |

| Total Assets | 898.71 | 893.26 | 1,031.14

|

Cash Flow Statement:

| Particulars (In Rs. Cr.) | FY20 | FY21 | FY22 |

| Cash Flow from Operating Activities | |||

| Profit from Operations | 105.00 | 159.00 | 259.00 |

| Receivables | 29.00 | -38.00 | -25.00 |

| Inventory | 15.00 | 14.00 | -103.00 |

| Payables | -17.00 | 32.00 | -1.00 |

| Other Working Capital items | 14.00 | 13.00 | 14.39 |

| Direct Taxes | -12.00 | -27.00 | -60.54 |

| Net Cash Flow from Operating Activities | 134.00 | 153.00 | 84.85 |

| Cash Flow from Investing Activities | |||

| Fixed Assets Purchased | -11.35 | -16.35 | -35.09 |

| Fixed Assets Sold | 0.00 | 1.08 | 0.41 |

| Interest Received | 1.24 | 0.78 | 0.88 |

| Other Investing Items | 2.12 | -2.98 | 1.43 |

| Net Cash Flow from Investing Activities | -7.99 | -17.47 | -32.37 |

| Cash Flow from Financing Activities | |||

| Proceeds from Borrowings | 0.00 | 0.00 | 0.40 |

| Repayment of Borrowings | -96.69 | -126.72 | -0.86 |

| Interest Paid | -15.60 | -7.18 | -4.65 |

| Dividends Paid | -6.53 | 0.00 | -40.49 |

| Financial Liabilities | -4.39 | -7.52 | -3.73 |

| Net Cash Flow from Financing Activities | -123.21 | -141.42 | -49.33 |

| Net Cash Flow for the Year | 2.80 | -5.89 | 3.15 |

| Key Ratios | FY20 | FY21 | FY22 |

| Debt to Equity | 0.78 | 0.45 | 0.26 |

| Current Ratio | 1.37 | 1.64 | 2.04 |

| ROCE (%) | 11.51 | 16.73 | 29.42 |

| ROE (%) | 14.14 | 17.84 | 27.15 |

| EBITDA Margin (%) | 14.09 | 18.15 | 22.13 |

| PAT Margin (%) | 6.9 | 10.1 | 13.75 |

Top Shareholders of UIL as of 31st December, 2022:

| Promoters | % Holding | FII | % Holding |

| Gurdeep Soni | 19.93% | Bnp Paribas Arbitrage – Odi | 1.25% |

| The Paramjit Soni 2018 CG-NG Nevada Trust (Through its Trustee Peak Trust Company-Nv) | 14.17% | The Nomura Trust And Banking Co., Ltd As The Trustee Of Nomura India Stock Mother Fund | 1.15% |

| The Karan Soni 2018 CG-NG Nevada Trust (Through its Trustee Peak Trust Company-Nv) | 9.08% | Icg Q Limited | 1.12% |

| The Meher Soni 2018 CG-NG Nevada Trust (Through its Trustee Peak Trust Company-Nv) | 9.08% | ||

| Angad Soni | 4.43% | ||

Peer Comparison:

UIL has no listed peer that operates in the similar business segments in which the company operates. However we can compare it to the other listed peers which have similar exposure to certain segments or use the similar nature of manufacturing process for their products.

Comparison of key parameters indicators for Fiscal 2022 with listed industry peers:

| Particulars | Uniparts India Ltd. | Balkrishna Industries Ltd. | Bharat Forge Ltd. | Ramkrishna Forgings Ltd. |

| Revenue from Operations (Rs.) | 1,227.42 | 8,295.12 | 10,461.08 | 2,320.25 |

| Net Profit (Rs.) | 168.78 | 1435.38 | 1081.76 | 198.03 |

| EBITDA (%) | 22.13 | 29.50 | 19.75 | 22.40 |

| Face Value (Rs.) | 10 | 2 | 2 | 2 |

| P/E (x) | 12.29 | 33.78 | 59.96 | 16.26 |

| EV/EBITDA | 0.53 | 17.91 | 16.75 | 7.90 |

| EPS (Rs.) | 45.40 | 60.65 | 13.76 | 16.45 |

| ROE (%) | 27.15 | 22.20 | 15.42 | 20.20 |

| ROCE (%) | 29.42 | 24.02 | 11.01 | 14.46 |

Outlook:

UIL is well-positioned with a significant market share in the global off-highway market and it is going to be benefitted further with the increasing mechanization in the agriculture, mining and forestry sectors globally. The strong distribution channel in the OEM and aftermarket segments will help the company to increase its customer base. Also company’s continuous focus on the new products and geographies along with leveraging its global business model will help it to maintain long term relationship with its clients. The operating environment in which the company is working shows signs of recovery be it Off-Highway vehicle industry growth or ease in global supply chain issues or cooling off in the commodity prices. The company has delivered strong financial performance over the years with Revenue CAGR of ~11% and PAT CAGR of 38.6% from FY20-FY22. It has delivered the EPS of Rs.36.07 for the nine months of FY23, and we expect it to exit the FY23 at eEPS of Rs.48.09. Hence, we recommend to buy the UIL at the current price of Rs.531 for the target price of Rs.670.

Source: Company website, EWL Research

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India.( SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Israil Khan, Elite Wealth Limited, suhail@elitewealth.in

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

(1) all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

(2) no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the report.

For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or emailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale.

Legal Entities Disclosures

Mr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone:011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

1. Reports

a) EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

(b) EWL or its associates or relatives, have no actual/beneficial ownership of one per cent. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

(c) EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

2. Compensation

(a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

(b) EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

(c) EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(d) EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(e) EWL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research report.

3 In respect of Public Appearances

(a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

(b) The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL