| Stocks Details | |

| Market Cap.(₹ Cr) | 3,16,685 |

| Equity (₹Cr) | 543 |

| Face Value (₹) | 2 |

| 52 Wk. high/low (₹) | 1,780.10/1,030 |

| BSE Code | 532281 |

| NSE Code | HCLTECH |

| Book Value (₹) | 294 |

| Industry | IT |

| P/E | 18.20X |

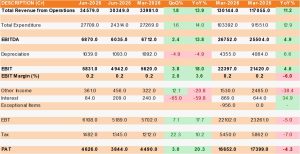

- Revenue from operations increased 13.9% YoY to ₹34,579 crore in Q1FY27 from ₹30,349 crore in Q1FY26 and grew 1.8% QoQ from ₹33,981 crore in Q4FY26. However, on a Constant Currency (CC) basis, revenue declined 0.5% QoQ while growing 2.6% YoY, reflecting the impact of AI-led disruption and cautious client spending across certain service lines.

- EBIT for the quarter stood at ₹5,831 crore, registering a growth of 18% YoY from ₹4,942 crore in Q1FY26 and 3.8% QoQ from ₹5,620 crore in Q4FY26. Consequently, the EBIT margin improved to 16.86%, expanding by 58 bps YoY from 16.28% and 32 bps QoQ from 16.54%.

- Profit after Tax (PAT) also witnessed healthy growth and stood at ₹4,626 crore in Q1FY27, up 20.3% YoY from ₹3,844 crore in Q1FY26 and stable 3% QoQ from ₹4,490 crore in Q4FY26.

- The company continued to strengthen its AI capabilities through strategic partnerships and investments. Advanced AI revenue reached $171 million during the quarter, growing 10.6% QoQ and 62.1% YoY on a Constant Currency basis. Annualized Advanced AI revenue has now reached $688 million, indicating that the company is aligning its business with the evolving AI landscape and positioning itself to capture long-term growth opportunities.

- Among business segments, IT and Business Services remained the largest contributor, generating ₹26,049 crore, accounting for nearly ~75% of total revenue. This was followed by Engineering and R&D Services with ₹5,690 crore (~ 16.5%) and HCL Software with ₹2,840 crore (~ 8.2%) during the quarter. On a Constant Currency basis, IT and Business Services recorded 4.2% YoY growth, Engineering and R&D Services 0.3% YoY up, while HCL Software declined 5.3% YoY. Among industry verticals, Financial Services continued to be the largest revenue contributor for the company.

- The Board declared an interim dividend of ₹12 per share, with the record date set for July 17, 2026, and the payment date on July 27, 2026.

- HCL Tech reported net new bookings of $2.4 billion during Q1FY27, marking the highest-ever first-quarter booking in the company’s history. The strong order inflow was broad-based across industries, service lines and geographies, providing healthy revenue visibility.

- HCL Software’s annual recurring revenue (ARR) stood at $1.063 billion, up 2% YoY in constant currency; however, software revenue declined 5.3% YoY while growing 2.2% sequentially, showing near-term volatility despite steady underlying ARR momentum in the segment.

- Geographically, the United States remained the company’s largest market, contributing ~ 56% of total revenue and registering 2.9% YoY growth. Europe contributed 27.6% of revenue and remained largely flat with 0.1% YoY growth. The Indian market accounted for 3.3% of revenue and delivered a strong 16.9% YoY growth, while the Rest of the World contributed 13.1% of revenue and reported 10.8% YoY growth, reflecting healthy traction across international markets outside North America and Europe.

- The company completed its acquisition of Jaspersoft, adding a visualization layer to its data management portfolio, enabling HCL Tech to convert governed, trusted data into actionable business insights closing a previously missing capability gap within its broader software and analytics stack.

- HCL Tech was selected by a Europe-headquartered Fortune Global 50 firm as technology partner for AI-led transformation of global digital workplace and enterprise network management, signaling continued success in winning large-scale, AI-anchored transformation mandates from top-tier global enterprise clients.

- HCL Tech announced a $151 million strategic investment in Sarvam, India’s sovereign full-stack AI company, aiming to combine Sarvam’s research depth with HCL’s enterprise relationships, engineering expertise, and software IP to build a differentiated full-stack AI platform across models and applications.

- LTM attrition remained stable at 12.7%, broadly consistent with recent quarters; management highlighted that revenue per employee has increased for five consecutive quarters up 3.3% YoY.

- Telecom vertical continues to see reduced discretionary spending with no signs of improvement over the past three months, while manufacturing particularly automotive remains under stress; conversely, retail and consumer vertical grew a strong 10% YoY on a major apparel client ramp-up.

- Engineering R&D Services (ERS) softness was directly linked to discretionary spending pressures, as ERS is reported as a distinct horizontal segment; management expects ERS to become a top growth driver again once discretionary technology spending broadly recovers across client end-markets.

Management Commentary and Guidance for FY27:

- Management reiterated its five-pillar AI strategy: transforming services proactively, building differentiated IP, expanding AI-led services, scaling AI partnerships, and developing AI talent—positioning HCL Tech to capture disproportionate share of AI-native and AI-amplified enterprise spending pools going forward.

- Management emphasized that smaller, specialized models trained on industry-specific data often deliver superior enterprise value versus large general-purpose models, being faster, more cost-efficient, and more accurate framing this as a leadership opportunity window that HCL intends to capture via Sarvam.

- HCL Tech unveiled a new AI Data Center business, committing an initial strategic investment of up to ₹3,500 crores, with ambitions to scale to 50 megawatts of capacity.

- Management clarified the AI data center investment is not a shift away from asset-light strategy but a targeted, asset-heavy move to secure scarce compute capacity, enabling higher-margin full-stack AI services encompassing GPUs, models, applications, and sovereign-assured managed service delivery.

- The company plans to leverage its own AI data center capacity to deliver managed services and outcome-based/fixed-price contracts more cost-effectively, given rising token costs are becoming a critical component of AI service delivery economics for global enterprise clients.

- FY27 guidance was at 1-4% company-level revenue growth and 1.5-4.5% services growth in constant currency, with EBIT margin guidance retained at 17.5-18.5%; importantly, this guidance excludes acquisitions, including the recently completed Jaspersoft deal and future inorganic contributions. And Management also expects order bookings to remain strong in Q2FY27.

- Management expects AI-led deflation of ~ 2-3% on the existing portfolio but maintains that underlying growth of 1-4% is sufficient to more than offset this deflationary pressure, resulting in net positive revenue growth despite productivity-driven pricing concessions to clients.

- India business contribution to overall revenue remains small 3.3% but is a strategic growth priority; management cited a $20 billion-plus AI opportunity in India and pointed to Sarvam as central to capturing sovereign AI demand from Indian enterprises and government

- West Asia/Middle East exposure remains minimal at under 0.5% of revenue; management confirmed some discretionary spending softness persisting from disruptions that began in March, though the direct financial impact on HCL Tech remains limited given the small regional exposure.

Outlook

HCL Tech is one of India’s leading IT services companies and is strategically strengthening its presence in Artificial Intelligence (AI) and data centre. To support this strategy, the company has entered into multiple partnerships and acquisitions while also announcing a ₹3,500 crore investment in data centres to expand its digital infrastructure capabilities.

The company reported muted sequential growth, with revenue increasing 1.8% QoQ and PAT rising 3% QoQ during Q1FY27. However, its AI business continued to witness strong momentum, with Advanced AI revenue reaching $171 million in the quarter, registering a 10.6% QoQ and 62.1% YoY growth on a Constant Currency basis. On an annualized basis, Advanced AI revenue has now reached $688 million, reflecting the company’s continued focus on building its AI capabilities in line with evolving industry trends.

During the quarter, HCL Tech reported new deal bookings of $2.4 billion, marking the highest-ever first-quarter deal intake in the company’s history and providing healthy revenue visibility for the coming quarters. Management has guided for FY27 revenue growth of 1%–4%, while the Services business is expected to grow 1.5%–4.5%. The company has also retained its EBIT margin guidance of 17.5%–18.5%.

Profit and Loss Statement:

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited (Elite Wealth Limited is wholly owned subsidiary of InCred Capital Financial Services Limited) does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India. (SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Vindhyachal Prasad, Elite Wealth Limited, vindhyachal@elitestock.com

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

All of the views expressed in the report accurately reflect his or her personal views about any and all of

the subject securities or issuers; and

No part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the report. For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or emailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale. Legal

Entities Disclosures

Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone: 011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

1.Reports

a)EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

b)EWL or its associates or relatives, have no actual/beneficial ownership of one %. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

c)EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

1.Compensation

- a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

b)EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

c)EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

d)EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

e)EWL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research report.

- In respect of Public Appearances

a)EWL or its associates have not received any compensation from the subject company in the past twelve months;

b)The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL