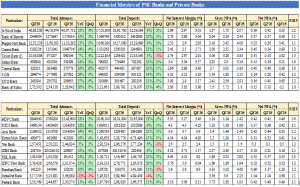

Public Sector Banks (PSU Banks) have clearly strengthened their positioning in the current cycle, with deposit and credit growth trends turning more favourable compared to several large private sector peers. Deposit mobilisation has been healthy and, in many cases, stronger than private banks, aided by their extensive branch network, deeper rural penetration, and improved customer confidence. CASA stability has supported funding costs, while credit growth has remained broad-based across retail, agriculture, MSME, and selective corporate lending. This balanced growth reflects disciplined underwriting and a more calibrated expansion strategy.

Asset quality remains one of the most constructive aspects for PSU banks. Gross and Net NPA ratios have steadily improved over the past few quarters, provision coverage ratios are comfortable, and fresh slippages remain contained. Compared to earlier cycles, balance sheets today are significantly cleaner, which enhances earnings visibility. The sustained improvement in asset quality provides confidence that PSU banks are structurally better placed to outperform over the near-to-long term horizon.

On the profitability front, PSU banks have emerged as relative outperformers. While private sector banks have delivered strong profitability over the last few years, there are early signs that margins may be normalising from peak levels (though it may be premature to draw firm conclusions). In contrast, PSU banks continue to show operating leverage benefits, controlled credit costs, and scope for further earnings expansion. We expect PAT growth for PSU banks to remain comparatively stronger over the coming quarters.

NIM outlook also appears relatively favourable for PSU banks. There is potential for modest margin improvement through better asset repricing and improved liability mix, whereas select private banks could see mild pressure due to elevated funding costs.

Valuations further support the investment case. Most PSU banks are trading at comfortable P/BV multiples of 1.0–1.5x (SBI around 2.2x), while major private sector heavyweights trade at richer valuations of 2.5x–3.1x. The combination of improving fundamentals, earnings momentum, and reasonable valuations presents an attractive risk-reward profile.