Market in 2022

Year 2022 was a volatile period for the Indian stock market with lots of global uncertainties with Ukraine-Russia war, Fed rate hikes, inflation and recession projections. The Indian market showed standout performance; NSE Nifty 50 index was up by 5.7% in the year, compared to the major global index average slump of 14%. Both key indices, Nifty 50 and BSE Sensex clocked their all-time high levels in December. Across sectors PSU banks have shown spectacular returns of 72%; Private banks, Metals, FMCG and Automobiles were some other sectors in the growing trajectory and were able to derive strong returns of 23%, 23.4%, 20% and 16.5% respectively. Worst sectors of the year were IT, Consumer durables, Pharma, Reality and Media.

The interest rate hikes by the RBI from 4.40% in May 2022 to 6.25% in December had impacted the market negatively. Another key trend for the sluggish market was soaring inflation; however the inflation rate dipped below the RBI’s tolerance level of 6% in November at 5.88% and offered some respite to the market.

Outlook for 2023

Going forward, we feel in 2023, market would not experience any significant downtrend but it might show slight turbulence because of the ongoing recession fear and high inflation. Sectors which could favor would be Banking and Financial services, Insurance, Infrastructure & allied sectors and Defence.

The domestic demand among sectors remains strong; being one of the youngest country in the world with median age of 28.7 years, domestic consumption among retail and IT would be resilient. Rising employment rate would be another driver for this demand. Banking sector would be major contributor in the upward direction for the market; rising interest rates and the gap between deposit and credit growth would aid the growth in BFSI. Infrastructure sector is also attributed to grow next year backed by several infrastructure projects in pipeline. Automobiles would sustain the growth momentum in 2023 due to rising EV adoption and new SUV launches. Reality sector is making a comeback after almost a decade and appears positive with the rising demand in the residential as well as commercial segments. Various PLI schemes catering to the automobile, defence, pharmaceuticals, textile & food sectors would support the long term growth of the Indian Economy.

In 2023, we can witness pressure on the highly leveraged companies due to the rising cost of borrowings hence we are expecting a balanced return from the markets. The long term investors should look any significant dip as an opportunity for the long term investment. India looks in a sweet spot but turbulence in between will continue and Investor should make full use of those dips.

New Year Stock Recommendations 2023

| Company | Sector | CMP (Rs.) | Target (Rs.) | Upside | Time Horizon |

| Asian Paints | Paints/Varnish | 3115 | 3675 | 18% | 12 months |

| Bharat Electronics | Electronics | 99 | 125 | 26% | 12 months |

| Cipla | Pharmaceuticals | 1088 | 1300 | 20% | 12 months |

| DLF | Construction | 373 | 450 | 21% | 12 months |

| HDFC Life Insurance | Insurance | 571 | 700 | 23% | 12 months |

| ICICI Bank | Banks – Private Sector | 908 | 1100 | 21% | 12 months |

| Infosys | IT – Software | 1518 | 1775 | 17% | 12 months |

| Mahindra & Mahindra | Automobiles | 1262 | 1450 | 15% | 12 months |

| Redington | Trading | 182 | 250 | 37% | 12 months |

| Reliance | Refineries | 2543 | 3200 | 26% | 12 months |

| SKF India | Bearings | 4541 | 5500 | 21% | 12 months |

| State Bank of India | Banks – Public Sector | 612 | 750 | 23% | 12 months |

New Year Stock Recommendations 2022

| Company | Recommended Price (Rs.) | Target (Rs.) | Target Status | High + Dividend | 52 Week High | Gains from High* |

| Reliance Industries | 2356 | 2950 | Target Almost Hit | 2885 | 2855 | 22.5% |

| Bharti Airtel | 676 | 920 | Position Closed | 880 | 877.10 | 30.2% |

| Larsen & Toubro | 1854 | 2320 | Position Closed | 2233 | 2210.50 | 20.4% |

| United Spirits | 888 | 1150 | Position Closed | 958 | 957.95 | 7.9% |

| Tata Motors | 464 | 585 | Position Closed | 528 | 528.35 | 13.9% |

| SBI Life Insurance | 1150 | 1440 | Position Closed | 1342 | 1339.55 | 16.7% |

| Infosys | 1858 | 2200 | Position Closed | 1986 | 1953.70 | 6.9% |

| Hindustan Unilever | 2305 | 2760 | Target Achieved | 2777 | 2741 | 20.5% |

| APL Apollo Tubes | 1011 | 1300 | Position Closed | 1197 | 1193.85 | 18.4% |

| Divi’s Laboratories | 4450 | 5400 | Position Closed | 4738 | 4707.80 | 6.5% |

*High + Dividend

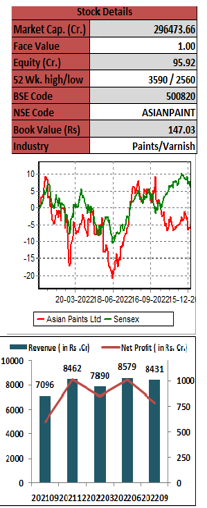

Asian Paints Limited (APL) is India’s largest and Asia’s third largest paint manufacturing company operating in 15 countries with 27 paint manufacturing facilities in the world. The company manufactures wide range of paints for decorative, automotive and industrial use. Apart from these the company also offers wall coverings, water proofing, adhesives and other services under its product portfolio. Company has started new range of hand, surface and space sanitizers and disinfectants and also recently launched range of Furniture, Furnishings and Lighting Products under ‘Home Décor’ category. Driven by its strong consumer focus and innovative spirit, the company has been the market leader in paints industry.

Key Takeaways:

• Announcement of strong capital expenditure plan of Rs. 6,750 crore over next three years for capacity expansion and backward integration.

• The home décor segment is delivering continuous growth. Company added 7 more stores in the Home Décor foray in the recent quarter, which was 29 in the previous year. The products and services offered under the segment is broadening. APL’s focus to become a full home décor player would make it a go-to brand in the home improvement space.

• The company boasts a wide and expansive distribution network including dealers and shopkeepers and also has a strong brand image among construction workers, which gives it a competitive edge among other players in the market.

• Decreasing trend in raw material price, positive GDP growth and ease in inflation would further improve the margins of the company in the periods ahead.

Outlook:

APL is the market leader in the Indian paint manufacturing industry and has major market share of more than 50% in the Indian decorative paint market. It has over 12,000 global workforce and has employed more than 200 scientists for the R&D work, which shows its continuous focus on the innovation. The company is strengthening its position for the future through acquisition and backward integration of imported raw materials requirements. Strong demand recovery in the automotive and industrial paints in the recent months due to construction work picking up; would be key driver for APL. On performance front the company’s TTM EPS is Rs. 39.26. The ROCE and ROE of the company is 28.80% and 23.18% respectively. Hence, we recommend to buy the stock at the current price of Rs.3115 for the target price of Rs.3675 with the time horizon of 12 months

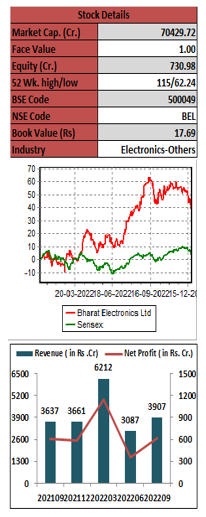

Bharat Electronics Limited (BEL) is a one of the leading public sector enterprise under the administrative control of the Department of Defence Production, Ministry of Defence. It manufactures and supplies wide range of electronic equipments and systems to defence sector and non-defence market. The company is a key player in the Indian Defence market and has a growing presence in the civilian and export segments. It exports products to Europe, Asia, Africa, North America, and the Middle East regions and has 6 overseas offices and 9 manufacturing units across India.

Key Takeaways:

• The company has strong aggregate order book value of Rs. 52,795 cr. (3.1 times of Trailing Twelve months Revenue) as of October 1, 2022 with an execution period of nearly 4 years, out of which Rs. 25,000-30,000 cr. is for naval business.

• BEL has formed many strategic alliances and partnerships with defence laboratories, reputed global OEMs and niche technology companies to address the emerging defence and non-defence business including exports.

• It has an export order book of Rs. 2,000 cr. which is moving aggressively also company is diversifying in other areas including civil aviation, metro rail business and energy storage products.

• The company has restated its Ebitda guidance to 22-23% from 21-23% earlier, and reiterated revenue growth guidance of 15% for FY23. It expects to log aggregate orders worth over Rs 20,000 cr. each in the current fiscal and in FY24.

Outlook:

BEL has established a strong competitive position in both defence and non-defence segments in the Indian and International markets. The company has shown growth and diversification over the years following the trend in electronics technology. It is emerging as a key beneficiary of the increase of defence capital expenditure. Ebitda margin would further increase due to the ease of chip supply situation globally. Company’s strategy to diversify into non-defence areas and focus on increasing exports and services would support long term growth. The TTM EPS of the company is Rs.3.75; it is currently delivering the ROCE & ROE of 23.55% and 20.17% respectively. BEL is trading at PE of 26.60x at the current price of Rs.99.75. Hence, we recommend to buy the stock at the current price for the target price of Rs.125 with the time horizon of 12 months.

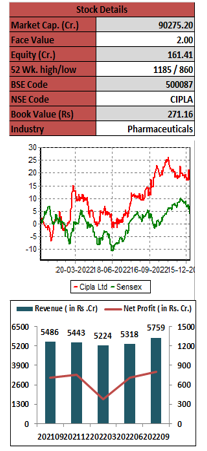

Cipla Limited (Cipla) is a leading pharmaceutical company from India with presence across the world. It is the 3rd largest pharmaceutical player in India and leader in therapies such as respiratory and urology and also ranked second in the overall chronic business. The company has a vast product portfolio with more than 1,500 products in various therapeutic categories. The company’s business is divided into three strategic units – APIs, respiratory and Cipla Global Access. Its largest market is India, followed by North America and Africa.

Key Takeaways:

• The company is continuously expanding its product portfolio and also scaling the positioning of its products into prescriptions, trade generics and consumer healthcare categories in India.

• Cipla has maintained its focus on its core strength of respiratory segment along with other complex generic pipeline in the US; this will bring significant momentum in the next few years.

• The management has guided Ebitda margin of 22% in 2HFY23 and is confident for the launch of g-Advair in 2HFY23. The company also expects the 505b2 approval for g-leuprolide acetate soon.

Outlook:

Cipla is in the business of manufacturing, developing, and marketing wide range of branded and generic formulations and Active Pharmaceutical Ingredients (APIs). Company has decent US launches in the pipeline; domestic business is also doing well. The rising demand for its drugs and inhalers would further drive this growth. Cipla has also acquired nutritional supplement maker Endura Mass, medical diagnostics firm Achira Labs and health tech company GoApptiv recently which would align the synergies for the company over longer term. On the performance front, the TTM EPS of the stock is at Rs. 32.14 and is trading at the PE of 33.77x at the current price level of Rs. 1085.50. We recommend to buy the stock at the current price for the target price of Rs.1300 with the time horizon of 12 months.

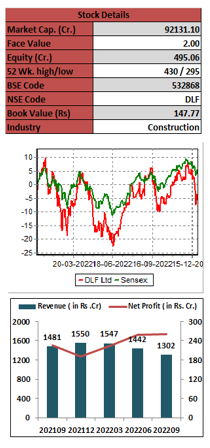

DLF Limited (DLF) is India’s largest real estate company in terms of revenues, earnings, market capitalisation and developable area. The operations of the company cover all aspects of real estate development, from the identification and acquisition of land, to planning, execution, construction and marketing of projects. Company has the track record of over 75 years and has developed more than 150 projects. It has presence in 22 cities, located in 14 States and Union Territories across India.

Key Takeaways:

• The company has strong launch pipeline with sales potential of ~ Rs.47,000 cr. across India with launch timeline of FY24 & beyond. These launches would help the company to maintain its top line growth in the period ahead.

• DLF has well diversified product mix across geographies and segments; low-rise development projects is leading to faster cash generation for the company.

• Its core residential business is showing strength, new sale bookings of the company grew significantly by 63% at Rs.4092 cr. in H1FY23 compare to the previous year Rs.2526 cr.

• Company is going to launch Rs.3500 cr. worth of new properties in the H2FY23 mainly in Gurugram and Panchkula to cater the rising demand in the sector.

Outlook:

DLF is the leading real estate developer in the country with the development potential of 215 msf across the residential and commercial segments. Its key projects include Cyber City, Cyber Sez, Cyber Park, Chennai Sez and Hyderabad Sez. The company is focusing on stronger cash generation through sustained momentum in sales. Demand for residential segment is witnessing continuous growth; shift in the customer preferences towards quality developments across residential and commercial space is another growth driver for the company. On the performance front, the TTM EPS of the stock is at Rs.6.60 and is trading at the PE of 56.57x at the current price level of Rs. 373.35. Hence, we recommend to buy the stock at the current price for the target price of Rs.420 with the time horizon of 12 months.

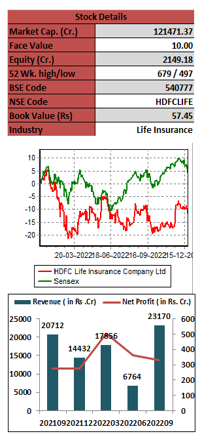

HDFC Life Insurance Limited (HLIL) is the leading private sector life insurers in India carrying on the business of life insurance. The Company offers a range of individual and group insurance solutions including participating, non-participating and unit linked lines of businesses. The portfolio comprises of various insurance and investment products such as Protection, Pension, Savings, Investment, Annuity and Health. It had Rs. 2,04,170 cr. of Asset under Management (AUM) in FY 21-22 and has currently 572 branches in India.

Key Takeaways:

• The company had delivered strong numbers in the recent quarter; Revenue increased by 12% Y-o-Y and Renewal premiums grew by 37% yearly.

• Merger with Exide Life would improve its geographical presence in Tier-II and Tier-III regions of South India.

• Company’s diversified product mix, continuous product innovation and large distribution network would be growth drivers in the long term.

• Indian Insurance industry remains hugely under penetrated at 3.2% in FY21 compared to other countries; company has huge opportunity to penetrate the underserviced segments.

Outlook:

HLIL is among the key players in the Indian life insurance market with a large distribution network and operation metrics. Company has leading VNB margin in the sector at 26.2% as of September 30, 2022. On an annualized premium equivalent (APE) basis, it reported significant increase of 42% yearly growth. Life Insurance business in India is poised to grow at double digit rate in terms of premium value. Large protection gap and increasing per capita income are key growth drivers for the sector and HLIL would likely to benefit with this growth. The TTM EPS of the company is at Rs. 6.85 and it is currently trading at the PE of 82.95x. Hence, we recommend to buy the stock at the current price of Rs.570 for the target price of Rs.700 with the time horizon of 12 months.

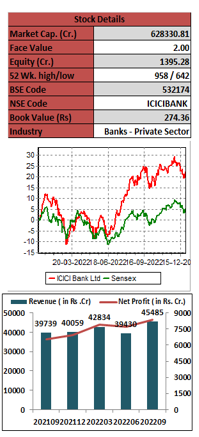

ICICI Bank Limited is one of the top private banks in the country offering a wide range of banking products and financial services to corporate and retail customers through its group companies. The bank has large network of 5,614 branches and 13,254 ATMs. It has a growing balance sheet and assets worth Rs. 14,886.74 cr. till September 30, 2022. The bank has diverse exposure in various sectors; top sectors are finance, banks, crude petroleum refining, electronics & engineering and infrastructure.

Key Takeaways:

• Asset quality of the bank has significantly improved. As of September 30, 2022, Gross retail, rural and business banking NPAs have declined by 138 bps from 3.26% to 1.88% and the Net retail, rural and business banking NPAs declined by 41 bps from 1.15% to 0.74% in the same quarter.

• Bank’s focus on transforming from a Bank to BankTECH and building strong technological infrastructure with continuous investment in innovations and security features would drive its growth further.

• ICICI Bank has continued to improve its retail, SME and business banking loan book; CASA ratio is at 45% in Q2FY23 and would likely to improve further in the rising interest rate environment.

Outlook:

ICICI bank has shown strong performance over the years despite the pandemic led disruptions. The bank increased its market share across key segments; UPI transactions is up by 2.2x in Q2FY23, also the number of credit cards grew by 13.68%. Currently it has the largest market share of 31% in FASTag (Electronic Toll Collections) in the industry. The bank’s liability has improved significantly, which is positive for its profitability and growth. Credit growth in the industry is accelerating giving the signs of industry revival also deposits of the bank would grow going forward as the gap of deposit rate and credit rate has widen recently. ICICI bank is trading at 21.15x at the current price level of 898.70; TTM EPS is at Rs. 42.5. Hence, we recommend to buy the stock at the current price of Rs.908 for the target price of Rs.1100 with the time horizon of 12 months.

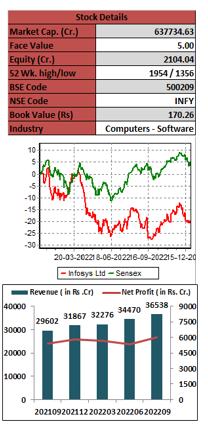

Infosys Ltd. is the 2nd largest IT sector company being the global leader in consulting, technology, outsourcing and next-generation digital services, enabling clients to create and execute strategies for their digital transformation. It offers services to various sectors comprising BFSI, retail, energy & utilities and communication contributing to ~ 31%, 14%, 12% and 12% respectively in the total revenue of the company. North America and Europe are the major revenue generating regions for Infosys.

Key Takeaways:

• The company reported strong operational performance with improving EBIT margins by 149 bps in Q2FY23 because of the better cost optimization and utilization.

• Attrition rate declined in the recent quarter to 27.1% Vs 28.4% earlier; company further expects the attrition rate to decline further in the period ahead.

• Management raised the revenue and margin guidance for FY23 to 15-16% and 21-23% reflecting the strong demand outlook despite the current headwinds in macro environment.

Outlook:

Infosys is one of the leading IT service giant in the world. Company services a large number of fortune 500 clients who have strong balance sheet. Further it is continuously adding large clients in its client lists. The strong relationship with these clients and strong execution capabilities keeps Infosys well positioned in the industry. Industry analysts estimate that IT services spending to grow by 8-8.5% in the next 4 years; Cloud infrastructure services & specialised software demand is further going to rise significantly. Infosys would be key beneficiary with the growth in the industry. The company is delivering the TTM EPS of Rs. 54.36 and is trading at the PE of 27.79x on the current price of 1510.85. We recommend to buy the stock for the target price of Rs.1775 with the time horizon of 12 months.

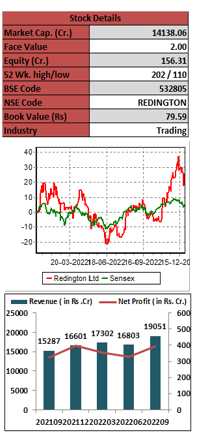

Redington Ltd. (Redington) is a leading supply chain solutions provider in the world, providing solutions to all categories of Information Technology, Telecom, Cloud, Lifestyle and Solar segment. The key business verticals of the company are Distribution, Services, Logistics Services and Emerging Businesses. It is a completely professionally managed company with no promoters and has expansive network of over 290+ brands association and 43,000+ channel partners. The company is currently serving to 38 emerging markets.

Key Takeaways:

• The company continuously focusing on the Cloud and IT service and has made a significant partnership with Google Cloud India to drive the cloud based services amongst the small and medium businesses (SMBs) in the country.

• Its solar business unit has recently made partnership with Enertech, a leading manufacturer of Solar Hybrid Inverter based in India to cater the rising demand in solar hybrid invertors in India.

• The company gets indirect benefit of the government’s Production Linked Incentive Scheme (PLI) for Electronics Manufacturing as it reduces imports and distributes more homemade products and is supporting the Make in India movement in the country.

Outlook:

Redington is emerging as the leading distributor for IT hardware and mobility products and providing complete platform for cloud solutions. It is also building India’s channel ecosystem for harnessing solar energy. The company is enhancing presence in the logistics business in India and the Gulf also the focus on the emerging cloud solutions would support the growth of the company. The business alignment with the demand of emerging technologies and solutions would be another key driver. The TTM EPS of Redington is Rs. 18.41; ROE and ROCE is 24.52% and 28.61% respectively. It is currently trading at the PE of 9.79x. Hence, we recommend to buy the stock at the current price for the target price of Rs.250 with the time horizon of 12 months.

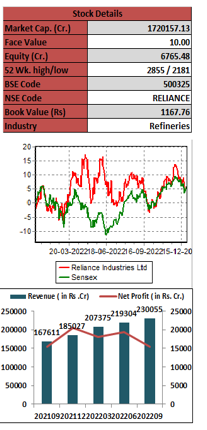

Reliance Industries Limited (RIL) is India’s largest private sector conglomerate with diversified businesses including energy, petrochemicals, natural gas, telecommunication and retail. The company has evolved from the textile and polyester company to an integrated player across energy, metals, petrochemical, retail, telecommunication and entertainment. It majorly operates through following segments: Oil to Chemicals (O2C), Oil & Gas, Retail, Digital Services, Financial Services, and Others. The company has been a major contributor in the development of the Indian Economy.

Key Takeaways:

• The recent windfall tax cut by the centre from Rs.4900 per tonne to Rs.1700 per tonne would help to maintain the bottom line; Oil & gas production would improve further as the company would commission new gas condensed field soon.

• Revenue of the Retail segment is continuously growing and the aggressive expansion plans through physical as well as digital platforms would bring long term growth further. Recent acquisition of Metro Cash & Carry India and Insight cosmetics would add more strength to its dominant position in the retail sector.

• Reliance Jio business is sequentially growing its market share and is at 36.85% in October 22 Vs 36.66% in September. Company is optimistic for its new energy business and is going to investing and acquiring thoroughly for the new energy ecosystem development.

Outlook:

RIL is engaged in activities spanning across hydrocarbon exploration and production, Oil to chemicals, retail, digital services and financial services. Retail, Telecom and new energy can be the next growth engines over the next decade for the company. The rollout of 5G services will further accelerate the ARPU for the Reliance Jio. The retail segment is strengthening; acquisition of several FMCG players by the company will help to gain the market share. RIL has given the EPS of Rs. 94.68 on TTM basis and is trading at the 26.85x on the current price of 2543. We recommend to buy the stock at the current price for the target price of Rs.3200 with the time horizon of 12 months.

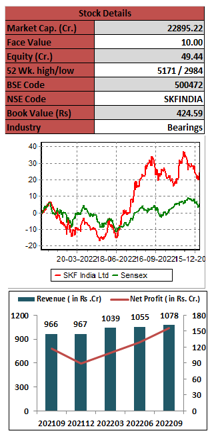

SKF India Limited (SIL) is one of the largest bearing manufacturer in India and is a part of AB SKF Germany group. The company’s product portfolio primarily consists of rolling bearing, seals, mechatronics, and lubrication systems. It has 3 manufacturing facilities, 12 offices and a supplier network of over 620 distributors. The company is a prominent supplier of ball bearings catering to over 40 industries across globe. The industries to which the company caters include automotive, railways, aerospace, agriculture, material handling, metals, construction, marine etc.

Key Takeaways:

• The company has shown strong financial performance over the years. Revenue CAGR and Profit CAGR for 5 years is at 7% and 10% respectively. It has zero debt and ROCE and ROE is at 29.97% and 22.9% respectively.

• Company is focusing to increase its presence in Tier 3 cities and increase its market share in the key segments.

• SKF has been focusing in the innovation and R&D; recent online market move and commencement of the dedicated freight corridor would play well for the company in the periods ahead.

Outlook:

SKF is one of the leading bearings manufacturer known for its deep groove ball bearings with a strong presence across the industrial and auto sectors. Industrial and auto segments have been contributing to ~ 50% each in the total revenue of the company over the years. The Indian bearings market is expected to grow at the CAGR of 10.9% by 2027 backed by the robust demand in construction, automotive and railway sector. Rising demand for high-precision bearings in specific applications will further boost this growth. SKF is well-poised to avail the benefits of rising growth in the industry. Currently the company is trading at the PE of 47.38 times and is delivering the EPS of Rs. 97.94. Hence, we recommend to buy the stock for the target price of Rs.5500 with the time horizon of 12 months.

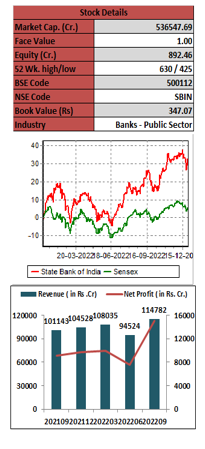

State Bank of India Limited (SBI) is India’s largest public sector bank operating from the last 40+ years with an extensive network of more than 22,266 branches, 65,030 ATMs & ADWMs (Automated Deposits Withdrawal Machine) and 232 international offices across 32 countries. It is a banking and financial services statutory body engaged in providing a wide range of products and services to individuals, commercial enterprises, large corporates, public bodies, and institutional customers. It has well diversified businesses operating through various subsidiaries i.e. SBI General Insurance, SBI Life Insurance, SBI Mutual Fund, SBI Cards etc.

Key Takeaways:

• The bank has shown robust operational and business growth in the Q2FY23. Asset quality of the bank has sequentially improved; GNPA and NNPA is at 3.52 Vs 4.9% and 0.8% Vs 1.52% in the year ago respectively.

• NIM of the bank is sequentially improving and is at 3.2% in the recent quarter; Bank is well playing the digital strategy, it has acquired 45% of retail assets accounts & 62% of savings accounts through YONO in Q2FY23.

• Bank has given the credit cost guidance of 14-16% led by strong demand across industries, which will further improve its business growth and overall performance.

Outlook:

SBI is the dominant player in the Indian banking sector being the largest bank in the public sector with 23% market share by assets. The bank has largest customer base in the country and has deep penetration in the rural and urban markets. It has significantly improved its balance sheet and has shown strong growth last two years. The bank expects healthy credit growth momentum to continue in FY23 across segments. The rising interest rate scenario would generate better margins further. On the performance front, SBI delivers TTM EPS of Rs. 46.14 and is trading at the PE of 13.03 times. We recommend to buy the stock for the target price of Rs.750 with the time horizon of 12 months.

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India.( SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Israil Khan, Elite Wealth Limited, suhail@elitewealth.in

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

(1) all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

(2) no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the report.

For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by

visiting https://www.elitewealth.in, or e-mailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, advisory board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale.

Legal Entities Disclosures

Mr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone:011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL Advisory discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

- Reports

- a) EWL Advisory or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

(b) EWL Advisory or its associates or relatives, have no actual/beneficial ownership of one per cent. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

(c) EWL Advisory or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

- Compensation

(a) EWL Advisory or its associates have not received any compensation from the subject company in the past twelve months;

(b) EWL Advisory or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

(c) EWL Advisory or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(d) EWL Advisory or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(e) EWL Advisory or its associates have not received any compensation or other benefits from the subject company or third party in connection with the research report.

3 In respect of Public Appearances

(a) EWL Advisory or its associates have not received any compensation from the subject company in the past twelve months;

(b) The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL Advisory

Provided that research analyst or research entity shall not be required to make a disclosure as per sub-clauses (c), (d) and (e) of clause (ii) or sub-clauses (a) and (b) of clause (iii) to the extent such disclosure would reveal material non-public information regarding specific potential future investment banking or merchant banking or brokerage services transactions of the subject company.

(4) EWL Advisory or its proprietor has never served as an officer, director or employee of the subject company;

(5) EWL Advisory has never been engaged in market making activity for the subject company;

(6) EWL Advisory shall provide all other disclosures in research report and public appearance as specified by the Board under any other regulations.