Dabur India Limited is among top four FMCG companies in India which offers consumer products such as hair care products, oral care products, healthcare products and food & beverages products. It has market leadership in the Honey, Chyawanprash, Air fresheners, Mosquito repellant creams and Juices in domestic business segment. The company has a large presence in rural India particularly in the northern and eastern part of India. Additionally, it has a substantial presence in the Middle East, North America and SAARC, which contributes about 25% of its overall revenue.

| Recommendation | PRICE RANGE | Target Price | Time Horizon |

| Accumulate | Rs. 480.00 -505.00 | Rs. 625 | 12 Months |

Stock Details |

|

| Market Cap. (Cr.) | 94547 |

| Equity (Cr.) | 177.20 |

| Face Value | 1 |

| 52 Wk. high/low | 597 / 504 |

| BSE Code | 500096 |

| NSE Code | DABUR |

| Book Value (Rs.) | 53.54 |

| Industry | FMCG |

| P/E | 52.72 |

Share Holding Pattern % |

|

Promoter |

66.24 |

| FIIs | 16.78 |

| Institutions | 11.78 |

| Non Promoter Corp. | 0.27 |

| Public & Others | 4.93 |

| Government | 0.00 |

| Total | 100.00 |

Key Investment Rationale:

-

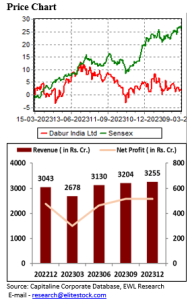

Dabur is a competitive player in the domestic market owing to its positioning as an Ayurvedic products company with a focus on herbal and natural products in the healthcare and personal care segments and a strong presence in the juices area. Furthermore, company’s international presence mitigates risk to its business model in case of demand slowdown in domestic market.

-

The company has continuously observed higher growth in rural regions compared to urban regions; In the Q3FY24, Rural growth stands at 6-6.5% compared to urban growth of about 5%. This revenue growth outperformance is expected to continue in the near future due to an improving volume trajectory and the absence of any impact from price reductions.

-

In the Q3FY24 results company announced capex of Rs.135 Cr. to establish a new Greenfield plant in South India and expanding the capacity for Red Toothpaste, Odonil, and Honey. Additionally with an eye on upcoming summer season, Dabur is expanding its beverage plant capacity through setting up a new plat in Indore for the drinks segment and in Jammu for aerated beverages.

-

Company’s Food & Beverages (F&B) business is demonstrating strong growth of 13% CAGR in the past 4 years which was driven by a 12.4% CAGR in the beverages segment and a 19.2% CAGR in the foods segment. The company is focused on to double the revenue from F&B business over the next five years. It is planning to expand the presence of recently acquired Badshah brand from the core markets of Maharashtra, Gujarat, Telangana and Andhra Pradesh to MP and Rajasthan.

Outlook:

Dabur India’s domestic business is expected to continue its growth momentum in the upcoming quarters, driven by market share gains in key categories, strong product launches and expansion in distribution reach. Company’s Healthcare, Home, and Personal care segments are expected to grow at high single-digit to low double-digit rates while Food and Beverages segment is expected to double over the next 4-5 years. Dabur is well placed to benefit from upcoming summer season, rural demand improvement along with moderation in inflation. Hence, we recommend investors to accumulate the company for the target price of 625 with the time horizon of 12 months.

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India.( SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Kiran Tahlani, Elite Wealth Limited, kirantahlani@elitestock.com

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

(1) all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

(2) no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the report.

For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or e-mailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale.

Legal Entities Disclosures

Mr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone: 011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

- Reports

- a) EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

(b) EWL or its associates or relatives, have no actual/beneficial ownership of one per cent. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

(c) EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

- Compensation

(a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

(b) EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

(c) EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(d) EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

(e) EWL or its associates have not received any compensation or other benefits from the subject company or third party in connection with the research report.

3 In respect of Public Appearances

(a) EWL or its associates have not received any compensation from the subject company in the past twelve months;

(b) The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL

Provided that research analyst or research entity shall not be required to make a disclosure as per sub-clauses (c), (d) and (e) of clause (ii) or sub-clauses (a) and (b) of clause (iii) to the extent such disclosure would reveal material non-public information regarding specific potential future investment banking or merchant banking or brokerage services transactions of the subject company.

(4) EWL or its proprietor has never served as an officer, director or employee of the subject company;

(5) EWL has never been engaged in market making activity for the subject company;

(6) EWL shall provide all other disclosures in research report and public appearance as specified by the Board under any other regulation