Avenue Supermarts Limited, headquartered in Mumbai, operates the D-Mart retail chain across India. D-Mart is a leading supermarket offering a comprehensive range of home and personal products. The Company’s product portfolio spans Foods, Non-Foods (FMCG), and General Merchandise & Apparel, including categories such as groceries, dairy, frozen foods, fresh produce, personal care, home essentials, apparel, footwear, and toys. As of June 30, 2025, Avenue Supermarts operated 424 stores (including one under renovation in Navi Mumbai) with a total retail business area of 17.6 million sq. ft. The stores are spread across key states and union territories, including Maharashtra, Gujarat, Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, and the National Capital Region (NCR), among others.

| Result Analysis: Avenue Supermarts Limited

(CMP: Rs. 4,020) |

Result Update: Q1FY26 |

| Stock Details | |

| Market Cap. (Cr.) | 2,61,660 |

| Equity (Cr.) | 651 |

| Face Value | 10 |

| 52 Wk. high/low | 5485/3337 |

| BSE Code | 540376 |

| NSE Code | DMART |

| Book Value (Rs) | 329.29 |

| Sector | Consumer Discretionary |

| Key Ratios | |

| ROCE (%): | 19.54 |

| ROE (%): | 14.58 |

| TTM EPS: | 41.60 |

| P/BV: | 12.20 |

| TTM P/E: | 96.63 |

| D/E | 0.04 |

Result Highlights:

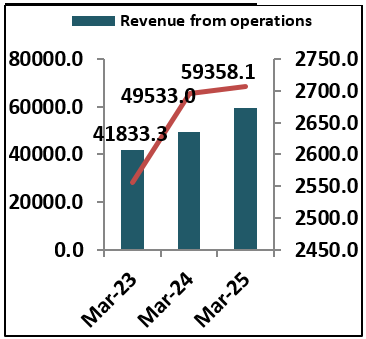

- D-Mart reported revenue from operations of Rs 16,359.70 crore for Q1 FY26, reflecting a YoY growth of 16.3% compared to Rs 14,069.14 crore in Q1 FY25. On a QoQ basis, revenue increased by 10% from Rs 14,871.86 crore in Q4 FY25. The revenue growth was moderated by significant deflation in several staples and non-food product categories.

- The company has reported an EBITDA of Rs 1,299.04 crore in Q1 FY26, marking a 6.4% YoY increase and a strong 36% QoQ growth from Rs 955.07 crore in Q4 FY25, indicating improved operational efficiency and cost management. And EBIDTA Margin for Q1FY26 7.94% declined from 8.68% in Q1FY25 and up from 6.42% in Q4FY25.

- Avenue Supermarts Ltd reported a Profit After Tax of Rs 772.81 crore for Q1 FY26, reflecting a marginal YoY basis decline of 0.1% compared to Rs 773.68 crore in Q1 FY25. However, on a QoQ basis, PAT registered a strong growth of 40% from Rs 550.79 crore in Q4 FY25.

- D-Mart follows Everyday low cost – Everyday low price (EDLC-EDLP) strategy which aims at procuring goods at competitive prices, using operational and distribution efficiency and thereby delivering value for money to customers by selling at competitive prices.

- The company added 9 new stores during the quarter, bringing the total store count to 424 as of June 30, 2025. This expansion reflects Avenue Supermarts Ltd’s continued focus on strengthening its retail footprint and enhancing accessibility across its key operating regions.

- In Q1 FY26, D-Mart generated 54.81% of its revenue from the Food segment, 20.30% from Non-Food (Non-FMCG), and 24.89% from General Merchandise and Apparel. This revenue mix highlights the company’s continued reliance on food retail while maintaining a balanced contribution from discretionary and non-FMCG categories.

Financial Performance:

Shareholding Pattern:

| Particulars (In %) | Q4FY25 | Q4FY24 |

| Promoter | 74.65 | 74.65 |

| FIIs | 8.29 | 8.37 |

| DIIs | 9.15 | 8.59 |

| Public and Other | 7.92 | 8.39 |

Management Commentary:

- Avenue Supermarts reported a 16.2% year-on-year growth in revenue for Q1 FY26, while PAT grew modestly by 2.1%. Comparable store sales (stores older than two years) grew by 7.1%. However, revenue growth was slightly impacted (by 100–150 basis points) due to significant deflation in staples and non-food categories.

- Gross margins declined compared to the same period last year, mainly due to intense competition in the FMCG segment. Additionally, operating costs increased as the company invested in service improvements, capacity expansion, and faced inflationary pressure on entry-level wages.

Outlook:

D-Mart reported healthy revenue growth in Q1 FY26 on both YoY and QoQ bases; however, both topline and bottom line missed market expectations. PAT declined marginally YoY, while revenue growth was impacted by significant deflation in staples and non-food categories. Gross margins were under pressure due to intensified competition in the FMCG segment. Despite these challenges, the company continued its expansion strategy by opening new stores during the quarter. D-Mart operates on the Everyday Low Cost – Everyday Low Price (EDLC-EDLP) model, focusing on procuring goods at competitive prices and leveraging operational efficiencies to offer consistent value to customers. The company reported a EPS of Rs 11.85 in Q1FY26 and TTM EPS of Rs 41.60 and currently trades at a TTM P/E of 96.63x and P/B of 12.20x.

Results:

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India.( SEBI Registration No.: INH100002300)Disclosure AppendixAnalyst Certification (For Reports)Vindhyachal Prasad, Elite Wealth Limited, vindhyachal@elitestock.comThe analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

- all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

- no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research ExcerptsThis note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.Company-Specific DisclosuresImportant disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or emailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.Options related research:If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.inOther DisclosuresAll research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.Ownership and material conflicts of interest DisclosureElite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of an y company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.Country Specific DisclosuresIndia – For private circulation only, not for sale. Legal Entities DisclosuresMr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone: 011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.inEWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

- Reports

- a) EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

- EWL or its associates or relatives, have no actual/beneficial ownership of one %. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

- EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

-

- Compensation

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

- EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

- EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research 3 In respect of Public Appearances

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

- The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL

| Particulars | Q1FY26 | Q1FY25 | Q4FY25 | YoY% | QoQ% | FY25 | FY24 | VAR [%] |

| Gross Sales | 16359.7 | 14069.1 | 14871.9 | 16.3 | 10.0 | 59358.1 | 50788.8 | 16.9 |

| Net Sales | 16359.7 | 14069.1 | 14871.9 | 16.3 | 10.0 | 59358.1 | 50788.8 | 16.9 |

| Other Income | 19.4 | 41.6 | 25.1 | -53.3 | -22.4 | 124.3 | 146.5 | -15.1 |

| Total Income | 16379.1 | 14110.7 | 14896.9 | 16.1 | 9.9 | 59482.4 | 50935.3 | 16.8 |

| Total Expenditure | 15060.7 | 12847.9 | 13916.8 | 17.2 | 8.2 | 54870.7 | 46685.1 | 17.5 |

| EBIDT | 1318.5 | 1262.9 | 980.1 | 4.4 | 34.5 | 4611.6 | 4250.2 | 8.5 |

| Interest | 29.3 | 16.0 | 19.0 | 83.6 | 54.5 | 69.5 | 58.1 | 19.5 |

| EBDT | 1289.2 | 1246.9 | 961.2 | 3.4 | 34.1 | 4542.2 | 4192.1 | 8.4 |

| Depreciation | 231.7 | 192.8 | 240.9 | 20.2 | -3.8 | 869.5 | 730.8 | 19.0 |

| EBT | 1057.5 | 1054.1 | 720.3 | 0.3 | 46.8 | 3672.7 | 3461.3 | 6.1 |

| Tax | 280.7 | 277.6 | 164.3 | 1.1 | 70.8 | 947.5 | 913.7 | 3.7 |

| Deferred Tax | 4.0 | 2.9 | 5.2 | 38.3 | -23.2 | 17.8 | 12.0 | 47.8 |

| PAT | 772.8 | 773.7 | 550.8 | -0.1 | 40.3 | 2707.5 | 2535.6 | 6.8 |