Bharat Electronics Limited (BEL) is a Navratna PSU under the Ministry of Defence, operating as a key beneficiary of India’s defence indigenization drive. The company specializes in manufacturing advanced electronic systems for the Army, Navy, and Air Force, while maintaining a strong presence in high-growth civilian and strategic verticals. Key non-defence segments include smart cities, homeland security, e-governance, space electronics, and satellite integration. Furthermore, BEL is capturing structural tailwinds in green mobility via EV charging stations and solar energy, alongside an expanding footprint in cybersecurity, telecom, medical electronics, and railway/metro solutions.

RecommendationAccumulate |

Accumulate Between₹410 – 380 |

Target Price₹ 495 |

Time Horizon9 – 12 Months |

| Stock Details | |

| Market Cap.(₹ Cr) | 3,01,346 |

| Equity (₹Cr) | 731 |

| Face Value | 1 |

| 52 Wk. high/low (₹) | 473.45/361.20 |

| BSE Code | 500049 |

| NSE Code | BEL |

| Book Value (₹) | 32.8 |

| Industry | Aerospace & Defense |

| P/E | 49.57x |

| Share Holding Pattern % | |

| FIIs | 19.5 |

| Institutions | 20 |

| Public | 9.4 |

| Government | 51.1 |

Price Chart

| Source: ACE Equity Nxt. and Company (mayor uniquoters ltd).

E-mail – research@elitestock.com |

Key Investment Rationale:

- As of 1 April 2026, BEL’s total order book stood at ₹73,882 crore, while order inflows during FY26 reached ₹30,045 crore, exceeding the company’s last annual guidance. The robust order backlog provides strong revenue visibility and supports sustainable growth.

- BEL is strengthening its presence in next-generation technologies, including Artificial Intelligence (AI), Quantum Computing, Quantum-Safe Communications, and Drone Electronics. And it follows a four-pillar collaborative ecosystem involving DRDO, technology start-ups, academic institutions, and in-house engineering teams, enabling accelerated innovation and indigenous technology development.

- The Indian government’s continued emphasis on defence modernization and higher defence budget allocations is expected to create significant opportunities for BEL, given its strong positioning across key defence electronics and strategic programs.

- BEL is targeting opportunities in the public data centre segment by integrating indigenous hardware, software stacks, and proprietary cybersecurity solutions developed in collaboration with C-DAC. The addressable opportunity in this segment is estimated at ₹2,000–10,000 crore.

- In collaboration with DRDO laboratories CHESS and MTRDC, BEL serves as the lead partner for the development of laser- and microwave-based Directed Energy Weapons (DEW). The company is also investing in localization initiatives through its Corporate R&D framework to enhance indigenous capabilities.

- Backed by recent localized computational upgrades, BEL is set to establish a brand-new, centralized high-performance computing infrastructure aimed at accelerating advanced domestic software modeling.

- It expects meaningful order inflows from India’s upcoming ₹90,000 crore P-75I submarine programme, where it aims to secure ~ 50–60% of the electronic subsystem requirements through its association with Mazagon Dock Shipbuilders Limited.

Q4FY26 and FY26 Results performance:

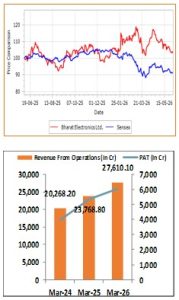

- Q4FY26 revenue from operations reached ₹10,224.4 Cr, up 42.9% QoQ from ₹7,153.9 Cr and 11.7% YoY from ₹9,149.6 Cr, driving full-year FY26 revenue up 16.2% YoY to ₹27,610.1 Cr from ₹23,768.8 Cr on the back of robust order execution.

- Q4FY26 PAT grew sharply by 40.9% QoQ and 4.7% YoY to ₹2,226.4 Cr from ₹1,579.7 Cr in Q3FY26 and ₹2,127.0 Cr in Q4FY25, leading to a strong 13.9% YoY expansion in full year FY26 PAT to ₹6,062.3 Cr from ₹5,322.7 Cr.

- The company has reported strong EBITDA for Q4FY26 of ₹2981.7 cr increased with the growth rate of 40.2% QoQ from ₹2127.2 cr in Q3FY26 and 5.9% YoY from ₹2816.1 cr in Q4FY25 and for FY26 also reported strong EBITDA and stood at ₹8049.3 cr up 17.8% as compared to ₹6833.8 cr in FY25.

- EBITDA margin decline of 57.2 bps QoQ in Q4FY26 from 29.7% in Q3FY26 to 29.2% in Q4FY26 and also down of 161.6 bps YoY from 30.8% in Q4FY25 but in terms of annual performance it has recorded 40.2 bps upside as compared to 28.8% in FY25 and reached at 29.2%, Q4FY26 margin decline due to input cost increased.

- It has announced an interim dividend of ₹1.95 per equity share and a final dividend of ₹0.55 per equity share for FY26, bringing the total dividend payout for the fiscal year to ₹2.50 per share.

FY27 Guidance & Management Outlook:

- Management has reaffirmed its guidance of more than 15% revenue growth for FY27, supported by a strong order backlog and the execution of major domestic defence programmes.

- BEL is targeting an EBITDA margin of over 28% in FY27, despite anticipated operational investments, evolving product mix, and continued focus on indigenous manufacturing.

- The company expects order inflows exceeding ₹55,000 crore in FY27, driven primarily by large air-defence and strategic defence contracts.

- BEL plans to invest approximately ₹2,200 crore in Research & Development (R&D) during FY27, with a strong focus on next-generation defence technologies and advanced platforms.

- Capital expenditure is projected to exceed ₹1,200 crore in FY27, representing more than 20% growth over the previous year. The investment will be utilized for capacity expansion, new facilities, and infrastructure upgrades.

- Management has maintained its revenue mix guidance at 90% defence and 10% non-defence, subject to minor revisions based on business developments during the year.

- Export revenues currently contribute around 4–5% of total revenue; however, management aims to increase this share to over 10% within the next five years, supported by strategic communication systems, satellite solutions, and customized C4I offerings for international markets.

Profit and Loss Statement:

| DESCRIPTION (₹ Cr) | Q4FY26 | Q3FY26 | Q4FY25 | QoQ% | YoY% | FY26 | FY25 | YoY % |

| Revenue from Operations | 10,224.4 | 7,153.9 | 9,149.6 | 42.9 | 11.7 | 27,610.1 | 23,768.8 | 16.2 |

| Total Expenditure | 7,242.7 | 5,026.7 | 6,333.5 | 44.1 | 14.4 | 19,560.8 | 16,935.0 | 15.5 |

| EBITDA | 2,981.7 | 2,127.2 | 2,816.1 | 40.2 | 5.9 | 8,049.3 | 6,833.8 | 17.8 |

| EBITDA Margin (%) | 29.2 | 29.7 | 30.8 | -1.9 | -5.2 | 29.2 | 28.8 | 1.4 |

| Depreciation | 173.0 | 135.4 | 137.6 | 27.7 | 25.7 | 555.7 | 467.4 | 18.9 |

| EBIT | 2,808.8 | 1,991.8 | 2,678.5 | 41.0 | 4.9 | 7,493.6 | 6,366.4 | 17.7 |

| Other Income | 110.2 | 138.5 | 194.6 | -20.4 | -43.4 | 566.0 | 742.4 | -23.8 |

| Interest | 1.6 | 2.0 | 5.9 | -20.0 | -72.9 | 6.7 | 9.7 | -30.9 |

| Share of (loss)/profit in A&JV | 12.2 | 9.5 | 6.0 | 28.4 | 103.3 | 38.8 | 35.5 | 9.2 |

| EBT | 2,929.6 | 2,137.8 | 2,873.2 | 37.0 | 2.0 | 8,091.8 | 7,134.6 | 13.4 |

| Tax | 703.2 | 558.1 | 746.2 | 26.0 | -5.8 | 2,029.5 | 1,811.9 | 12.0 |

| PAT | 2,226.4 | 1,579.7 | 2,127.0 | 40.9 | 4.7 | 6,062.3 | 5,322.7 | 13.9 |

| EPS | 3.04 | 2.16 | 2.91 | 40.74 | 4.47 | 8.29 | 7.28 | 13.87 |

Outlook:

BEL is one of India’s leading defence electronics companies, developing and manufacturing advanced technology systems and equipment for the Army, Navy, and Air Force. While defence remains its core business, the company is also expanding its presence in high-growth segments such as cybersecurity, smart cities, and clean energy solutions.

It has ended Q4FY26 and FY26 on a strong note, Driven by robust order book execution, Q4FY26 revenue from operations grew by 42.9% QoQ, while PAT surged by 40.9% QoQ compared to Q3FY26. On annual front, the company maintained strong momentum, with top-line growing by 16.2% and the bottom line expanding by 13.9% over FY25.

BEL secured strong order inflows of ₹30,045 Cr in FY26, taking its total order book to ₹73,882 Cr. Management is confident of maintaining this momentum into FY27, targeting order inflows exceeding ₹55,000 Cr. Additionally, the company is actively exploring diversification opportunities within the high-growth data center segment.

For FY27, management has provided a strong revenue growth guidance of 15% alongside stable EBITDA margins of 28%. To support this growth, a strategic capital expenditure plan has been laid out for FY27, allocating ~₹2,200 Cr toward R&D and ~₹1,200 Cr for capacity expansion and infrastructure.

Valuation and Investment Recommendation: BEL reported an EPS of ₹8.29 for FY26. At the CMP of ₹411, the stock trades at a P/E multiple of 49.57x. Given the company’s strong revenue visibility, robust order book, and clear growth catalysts, we believe that the valuation is fair at the current level. Thus, we recommend investors to ACCUMULATE BEL between the ₹410 – 380 range for a target price of ₹495, with a time horizon of the next 9–12 months.

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India. (SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Vindhyachal Prasad, Elite Wealth Limited, vindhyachal@elitestock.com

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

- all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

- No part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or emailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale. Legal Entities Disclosures

Mr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone: 011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

- Reports

- a) EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

- EWL or its associates or relatives, have no actual/beneficial ownership of one %. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

- EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

- Compensation

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

- EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

- EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research

- In respect of Public Appearances

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL