| Result Analysis: Billionbrains Garage Ventures Ltd (Groww) (CMP: ₹214) | Result Update Q4FY26 |

| Stock Details | |

| Market Cap. (₹Cr.) | 1,34,286 |

| Equity (₹Cr.) | 1,254.72 |

| Face Value (₹) | 2 |

| 52 Wk. high/low | 218 / 112 |

| BSE Code | 544603 |

| NSE Code | GROWW |

| Book Value (₹) | 15.40 |

| Sector | FINANCIAL SERVICES |

Result Highlights:

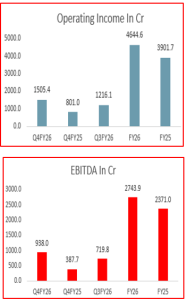

- Revenue from operations witnessed strong growth of 23.8% QoQ, reaching ₹1,505.4 crore in Q4FY26 from ₹1,216.1 crore in Q3FY26, and grew 87.9% YoY from ₹801 crore in Q4FY25. For FY26, revenue stood at ₹4,644.6 crore, registering a robust growth of 19.0% YoY compared to ₹3,901.7 crore in FY25, led by equity derivative segment.

- EBITDA performance remained strong, standing at ₹938 crore in Q4FY26, reflecting a robust growth of 30.3% QoQ from ₹719.8 crore in Q3FY26 and 141.9% YoY from ₹387.7 crore in Q4FY25. On an annual basis, EBITDA stood at ₹2,743.9 crore in FY26, marking a healthy growth of 15.7% YoY compared to ₹2,371.0 crore in FY25

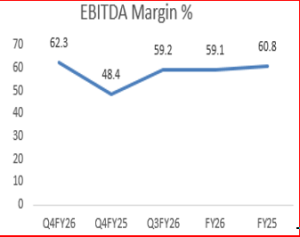

- EBITDA margin remained strong at 62.3% in Q4FY26, expanding by 3.1 bps QoQ from 59.2% in Q3FY26 and 13.9 bps YoY from 48.4% in Q4FY25. However, on a full year basis, EBITDA margin stood at 59.1% in FY26, marginally declining by 1.7 bps compared to 60.8% in FY25.

- PAT posted robust growth, increasing 25.5% QoQ to ₹686.4 crore in Q4FY26 from ₹546.9 crore in Q3FY26 and surging 122.1% YoY from ₹309.1 crore in Q4FY25. On a yearly basis, PAT stood at ₹2,083 crore in FY26, registering a healthy growth of 14.2% YoY compared to ₹1,824.4 crore in FY25.

- Groww continued to witness strong user and activity growth in Q4FY26, driven by sustained momentum in new user acquisitions and higher engagement across products.

- Active users grew 19.9% YoY and 4.7% QoQ in Q4FY26 to 16.7 million, reflecting continued traction from Q3, while total transacting users stood at 21.6 million, up 25% YoY and 6% QoQ. Total customer assets increased 36% YoY, but declined 1.1% QoQ due to MTM impact, despite robust customer activity driven by higher adoption of new products and increased usage of existing offerings. Net inflows remained strong at ₹25,000 crore during the quarter; however, MTM movements led to a decline of ₹3,300 crore in total customer assets

- In Mutual Funds, new SIP registrations witnessed strong growth of 61.5% YoY and 10.4% QoQ, while SIP inflows remained robust, increasing 34.8% YoY and 5.6% QoQ to ₹13,023 crore, with a 14% market share, outperforming industry growth of 18.7% YoY and 3.3% QoQ.

- In the Stocks segment, turnover per user increased 25.4% YoY and 13.8% QoQ, while active users grew 18.8% YoY and 3.5% QoQ, indicating healthy trading activity. Additionally, retail cash ADTO witnessed strong growth of 53.9% YoY, reaching ₹13,791 crore in Q4FY26 compared to ₹8,961.5 crore in Q4FY25, with a market share of 15.7%.

- In Equity Derivatives, performance remained strong, with average orders per user growing 43.1% YoY and 8.7% QoQ, while active users increased 21.7% YoY and 14.7% QoQ, led by rising participation. Additionally, Retail Derivatives Premium ADTO witnessed robust growth of 109.1% YoY, reaching ₹16,493.3 crore in Q4FY26 compared to ₹7,887.1 crore ¬in Q4FY25, with a market share of 10.6%

- New segments such as Commodity Derivatives, Margin Trading Facility (MTF), and LAS continued to gain strong traction, driven by increasing penetration and user adoption. These segments are scaling up meaningfully and contributing to overall growth.

- MTF book grew 22% QoQ in Q4, adding ₹506.9 crore and a 7% contraction in industry MTF book, leading to market share gains. While growth is market-linked, there remains significant scope to scale further, even in volatile conditions.

- In Commodity Derivatives, average daily orders witnessed a sharp growth of 60.7% QoQ, reflecting strong momentum. While the segment remains at an early stage, active users increased to 393K (+53.8% QoQ), indicating rising adoption, with an attach rate of 2.4% of total active users.

Management Commentary:

- Going forward, revenue growth is expected to drive margin expansion. If revenue growth sustains at 15% or above, margins are likely to improve gradually along with business scale.

- The core focus remains helping customers build long-term wealth, and this continues to guide its strategy and decision-making across products and services.

- The approach is to keep scaling core businesses and gain market share, as this strategy has worked well in the past and remains central to overall growth plans.

- Artificial Intelligence is expected to play a bigger role, especially in improving customer experience and increasing team productivity, helping the company launch better products faster.

- The industry environment has improved compared to earlier, but a clear growth cycle will depend on consistent FII inflows, which are still being monitored closely.

- During the quarter, market volatility remained high due to global factors, which boosted activity in derivatives and commodities, but also resulted in higher risk-related costs.

- Even though Indian capital markets have grown significantly, penetration is still low, leaving a large long-term opportunity with potential to grow 3–4x over the next decade.

- Groww’s asset management business (Groww MF) is still at a very early stage and currently operates at a sub-scale level. For the business to turn profitable, AUM needs to grow 5–6x, which is expected to be achieved over the next few year

Outlook

Groww has delivered a strong financial performance both quarterly and annually, with revenue from operations growing 23.8% QoQ in Q4FY26 and 87.6% YoY in FY26 compared to FY25. Profitability also remained healthy, with PAT growing 14.2% YoY, led by strong performance across all segments.

The platform continues to gain traction, with active users and transacting users increasing to 16.7 million and 21.6 million, respectively, indicating rising market share across segments. SIP inflows and new SIP registrations also showed strong momentum, with total net inflows of around ₹25,000 crore during the period.

Going ahead, the company is targeting revenue growth of 15% or higher, while maintaining its core focus on long-term wealth creation for investors. Additionally, the AMC business is expected to grow 5–6x over the next few years, which could help turn this segment profitable.

It reported an EPS of ₹3.40 in FY26 and is currently trading at a CMP of ₹212, implying a P/E multiple of 62.94x. While the valuation appears elevated relative to typical benchmarks, the company’s strong financial performance and clear growth visibility provide a degree of justification for the premium.

Given its solid fundamentals and favorable outlook, the company is well-positioned to deliver outperformance over the medium to long term.

Results:

| Particulars (In Cr) | Q4FY26 | Q4FY25 | Q3FY26 | QoQ% | YoY% | FY26 | FY25 | YoY % |

| Operating Income | 1505.4 | 801.0 | 1216.1 | 23.8 | 87.9 | 4644.6 | 3901.7 | 19.0 |

| Other Income | 30.17 | 48.57 | 45 | -33.0 | -37.9 | 171.3 | 159.92 | 7.1 |

| Total Income | 1535.54 | 849.57 | 1261.07 | 21.8 | 80.7 | 4815.88 | 4061.65 | 18.6 |

| Operating Expenditure | ||||||||

| Interest | 8 | 15.93 | 10.5 | -23.8 | -49.8 | 45.94 | 42.55 | 8.0 |

| Employee Expenses | 173.4 | 120.05 | 157.05 | 10.4 | 44.4 | 590.83 | 315.18 | 87.5 |

| Other Expenses | 393.98 | 293.25 | 339.2 | 16.1 | 34.3 | 1309.82 | 1215.54 | 7.8 |

| TOTAL OPERATING EXPENDITURE | 575.38 | 429.23 | 506.75 | 13.5 | 34.0 | 1946.59 | 1573.27 | 23.7 |

| Operating Profit Before Prov. & Cont. | 960.16 | 420.34 | 754.32 | 27.3 | 128.4 | 2869.29 | 2488.38 | 15.3 |

| Depreciation | 24.46 | 6.64 | 9.48 | 158.0 | 268.4 | 47.87 | 24.6 | 94.6 |

| TOTAL EXPENDITURE | 599.84 | 435.87 | 516.23 | 16.2 | 37.6 | 1994.46 | 1597.87 | 24.8 |

| PBT | 935.7 | 413.7 | 744.85 | 25.6 | 126.2 | 2821.41 | 2463.78 | 14.5 |

| Tax | 268.55 | 101.14 | 200.71 | 33.8 | 165.5 | 770.24 | 616.31 | 25.0 |

| Deferred Tax | -19.21 | 3.46 | -2.79 | 588.5 | -655.2 | -31.83 | 23.1 | -237.8 |

| PAT | 686.4 | 309.1 | 546.9 | 25.5 | 122.1 | 2083.0 | 1824.4 | 14.2 |

Source: Company website, EWL Research

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited (Elite Wealth Limited is wholly owned subsidiary of InCred Capital Financial Services Limited) does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India. (SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Vindhyachal Prasad, Elite Wealth Limited, vindhyachal@elitestock.com

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

- All of the views expressed in the report accurately reflect his or her personal views about any and all of

the subject securities or issuers; and

- No part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or emailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of any company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale. Legal

Entities Disclosures

Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone: 011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

- Reports

- EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

- EWL or its associates or relatives, have no actual/beneficial ownership of one %. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

- EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

- Compensation

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

- EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

- EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research

- In respect of Public Appearances

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

- The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL