Hero MotoCorp Limited primarily engages in the manufacture and sale of motorized two-wheelers across India, Asia, Central and Latin America, Africa, and the Middle East. The company offers a wide range of motorcycles, scooters, and electric scooters, along with engines, parts, accessories, and related services. Formerly known as Hero Honda Motors Ltd., it was renamed Hero MotoCorp Limited in July 2011.

| Result Analysis: Hero MotoCorp Limited

(CMP: Rs. 4,051) |

Result Update: Q4FY25 |

| Stock Details | |

| Market Cap. (Cr.) | 81021 |

| Equity (Cr.) | 40 |

| Face Value | 2 |

| 52 Wk. high/low | 6246/3323 |

| BSE Code | 500182 |

| NSE Code | HEROMOTOCO |

| Book Value (Rs) | 963.55 |

| Sector | Automobile |

| Key Ratios | |

| ROCE (%): | 29.47 |

| ROE (%): | 22.71 |

| EPS: | 218.69 |

| P/BV: | 4.2 |

| P/E: | 18.52 |

| D/E | 0.02 |

Result Highlights:

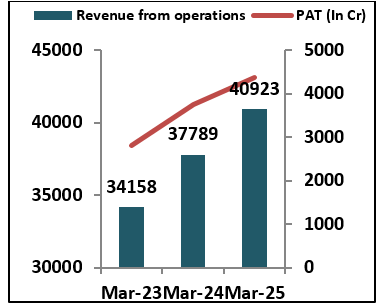

- Reported Revenue from operations in Q4FY25 of Rs 9969.81 cr increased with the growth rate of 3.7% from Rs 9616.68 cr in Q4FY25 on YoY basis and but decreased 2.8% from Rs 10259.89 cr in Q3FY25 on QoQ basis.

- It has reported EBIDTA for Q4FY25 of Rs 1440.75 cr up 9.2% from Rs 1319 cr in Q4FY24 on YoY basis and up 1.74% from Rs 1415.98 cr in Q3FY25 on QoQ basis. And EBIDTA margin of 14.45% in Q4FY25 improved from 13.72% in Q4FY24 on YoY basis and also improve on QoQ basis from 13.80% in Q3FY25.

- Hero Motor has reported PAT during Q4FY25 of Rs 1168.75 cr reflected growth rate of 23.9% from Rs 943.46 cr in Q4FY24 on YoY basis and up 5.4% from Rs 1108.38 cr in Q3FY25 on QoQ basis.

- Hero MotoCorp recorded volumes of 13.81 lakh units in Q4 FY25 as compare to 13.92 lakh units in Q4FY24, while total volumes for the full fiscal year FY25 stood at 58.399 lakh units as compare to 56.21 lakh units in FY24.

- Hero MotoCorp has completed the acquisition of a 34.10% stake in Euler Motors, making it an associate company. Alongside Ather Energy, this strategic investment is expected to strengthen Hero’s electric mobility portfolio.

- Especially in the new premium and scooter offerings, continued consolidation in the core segment, growth in the 125cc category, and the upcoming EV launch position well for sustained momentum.

- The company continued to push forward with its premiumiztion strategy, launching several new high-end models during FY25, including the Xtreme R, Xpluse , and the 2024 edition of the Xtreme 160R 2V. Additionally, Hero MotorCorp reinforced its presence in the scooter segment with the introductions of the new Destini 125, Xoom 125, and Xoom 160.

- Hero MotorCorp also achieved its highest-ever electric vehicle sales, recording nearly a 200% increase compare to FY24, futher solidifying its commitment the growing EV market.

Financial Performance:

Shareholding Pattern:

| Particulars (In %) | Q4FY25 | Q4FY24 |

| Promoter | 34.74 | 34.76 |

| FIIs | 27.80 | 29.27 |

| DIIs | 27.91 | 27.76 |

| Public & Other | 9.56 | 8.21 |

Management Commentary:

- Hero MotoCorp expects the two-wheeler industry to grow at a mid-to-high single-digit rate in FY26 (6%-7%). The company has recorded consistent month-on-month market share gains in FY25 and is witnessing a recovery in demand for commuter motorcycles.

- It has announced dividend of Rs 65 per share, total dividend of Rs 165 per share.

- The company remains optimistic about the near-to-mid-term outlook, with key macroeconomic indicators—such as revised income tax slabs, potential repo rate cuts, a strengthening rural economy, and a favorable monsoon forecast—expected to support industry growth.

Outlook:

Hero MotoCorp remains optimistic about its growth prospects in FY26, supported by favorable macroeconomic indicators such as revised income tax slabs, potential repo rate cuts, a strengthening rural economy, and a positive monsoon forecast. The company expects the two-wheeler industry to grow at a mid-to-high single-digit rate and anticipates continued recovery in commuter motorcycle demand. Strategic investments in electric mobility, including stakes in Ather Energy and Euler Motors, are expected to enhance its EV portfolio. With consistent gains in market share and improved operational performance. It has posted an EPS of Rs 218.69 in FY25. The stock currently trading at a P/E of 18.52x and P/B of 4.2x.

Results:

| Particulars (In Rs. Cr.) | Q4FY25 | Q4FY24 | Q3FY25 | YoY% | QoQ% | FY25 | FY24 | YoY% |

| Sales | 9969.81 | 9616.68 | 10259.89 | 3.7 | -2.8 | 40923.42 | 37788.62 | 8.3 |

| Other Income | 345.23 | 177.33 | 306.42 | 94.7 | 12.7 | 1044.08 | 854.54 | 22.2 |

| Total Income | 10315.04 | 9794.01 | 10566.31 | 5.3 | -2.4 | 41967.5 | 38643.16 | 8.6 |

| Total Expenditure | 8529.06 | 8297.68 | 8843.91 | 2.8 | -3.6 | 35138.7 | 32719.23 | 7.4 |

| EBIDT | 1785.98 | 1496.33 | 1722.4 | 19.4 | 3.7 | 6828.8 | 5923.93 | 15.3 |

| Interest | 16.93 | 7.64 | 16.55 | 121.6 | 2.3 | 70.65 | 76.37 | -7.5 |

| EBDT | 1769.05 | 1488.69 | 1705.85 | 18.8 | 3.7 | 6758.15 | 5847.56 | 15.6 |

| Depreciation | 204.14 | 196.61 | 208.91 | 3.8 | -2.3 | 824.59 | 757.36 | 8.9 |

| EBT | 1564.91 | 1292.08 | 1496.94 | 21.1 | 4.5 | 5933.56 | 5090.2 | 16.6 |

| Tax | 369.87 | 331.03 | 363.64 | 11.7 | 1.7 | 1448.02 | 1264.18 | 14.5 |

| Deferred Tax | 26.29 | 17.59 | 24.92 | 49.5 | 5.5 | 109.73 | 83.86 | 30.8 |

| PAT | 1168.75 | 943.46 | 1108.38 | 23.9 | 5.4 | 4375.81 | 3742.16 | 16.9 |

Source: Company website, EWL Research

Disclosure in pursuance of Section 19 of SEBI (RA) Regulation 2014

Elite Wealth Limited does/does not do business with companies covered in its research reports. Investors should be aware that the Elite Wealth Limited may/may not have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only information in making their investment decision and must exercise their own judgment before making any investment decision.

For analyst certification and other important disclosures, see the Disclosure Appendix, or go to www.elitewealth.in. Analysts employed by Elite Wealth Limited are registered/qualified as research analysts with SEBI in India.( SEBI Registration No.: INH100002300)

Disclosure Appendix

Analyst Certification (For Reports)

Vindhyachal Prasad, Elite Wealth Limited, vindhyachal@elitestock.com

The analyst(s) certify that all of the views expressed in this report accurately reflect my/our personal views about the subject company or companies and its or their securities. I/We also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. Unless otherwise stated, the individuals listed on the cover page of this report are analysts in Elite Wealth Limited.

As to each individual report referenced herein, the primary research analyst(s) named within the report individually certify, with respect to each security or issuer that the analyst covered in the report, that:

- all of the views expressed in the report accurately reflect his or her personal views about any and all of the subject securities or issuers; and

- no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in the For individual analyst certifications, please refer to the disclosure section at the end of the attached individual notes.

Research Excerpts

This note may include excerpts from previously published research. For access to the full reports, including analyst certification and important disclosures, investment thesis, valuation methodology, and risks to rating and price targets, please visit www.elitewealth.in.

Company-Specific Disclosures

Important disclosures, including price charts, are available and all Elite Wealth Limited covered companies by visiting https://www.elitewealth.in, or emailing research@elitestock.com with your request. Elite Wealth Limited may screen companies based on Strategy, Technical, and Quantitative Research. For important disclosures for these companies, please e-mail research@elitestock.com.

Options related research:

If the information contained herein regards options related research, such information is available only to persons who have received the proper option risk disclosure documents. For a copy of the risk disclosure documents, please contact your Broker’s Representative or visit the OCC’s website at https://www.elitewealth.in

Other Disclosures

All research reports made available to clients are simultaneously available on our client websites. Not all research content is redistributed, e-mailed or made available to third-party aggregators. For all research reports available on a particular stock, please contact your respective broker’s sales person.

Ownership and material conflicts of interest Disclosure

Elite Wealth Limited policy prohibits its analysts, professionals reporting to analysts from owning securities of an y company in the analyst’s area of coverage. Analyst compensation: Analysts are salary based permanent employees of Elite Wealth Limited. Analyst as officer or director: Elite Wealth Limited policy prohibits its analysts, persons reporting to analysts from serving as an officer, director, board member or employee of any company in the analyst’s area of coverage.

Country Specific Disclosures

India – For private circulation only, not for sale. Legal Entities Disclosures

Mr. Ravinder Parkash Seth is the Managing Director of Elite Wealth Ltd (EWL, henceforth), having its registered office at Casa Picasso, Golf Course Extension, Near Rajesh Pilot Chowk, Radha Swami, Sector-61, Gurgaon-122001 Haryana, is a SEBI registered Research Analyst and is regulated by Securities and Exchange Board of India. Telephone: 011-43035555, Facsimile: 011-22795783 and Website: www.elitewealth.in

EWL discloses all material information about itself including its business activity, disciplinary history, the terms and conditions on which it offers research report, details of associates and such other information as is necessary to take an investment decision, including the following:

- Reports

- a) EWL or his associate or his relative has no financial interest in the subject company and the nature of such financial interest;

- EWL or its associates or relatives, have no actual/beneficial ownership of one %. or more in the securities of the subject company, at the end of the month immediately preceding the date of publication of the research report or date of the public appearance;

- EWL or its associate or his relative, has no other material conflict of interest at the time of publication of the research report or at the time of public appearance;

- Compensation

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

- EWL or its associates have not managed or co-managed public offering of securities for the subject company in the past twelve months;

- EWL or its associates have not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months;

- EWL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research 3 In respect of Public Appearances

- EWL or its associates have not received any compensation from the subject company in the past twelve months;

- The subject company is not now or never a client during twelve months preceding the date of distribution of the research report and the types of services provided by EWL